Why 90% of Dividend Investors Fail (And How to Join the Top 10%)

Only Two Critical Moves Separate the Winners from the Losers

In 2008, while others pawned their belongings to pay rent, my dividend checks rolled in—like clockwork.

Yes, I’m living on dividends. They cover my mortgage, my car, and the occasional trip to Hawaii. And they kept growing—even during the last recession.

Last year alone, my dividend system handed me a 12% raise.

Yet, I see too many “dividend investors” see a 7% yield and jump in blind.

Then, they blame the strategy.

I’ve coached hundreds of investors to build bulletproof portfolios —and now it’s your turn.

Let’s talk about the biggest mistakes dividend chasers make—and how to fix them.

FAST.

Mistake #1: Chasing Yield like its Bitcoin in 2017

High yields are often compensation for risk, not generosity. Companies dangling 6%+ yields are usually drowning in debt, facing declining earnings, or both.

AT&T (T): Slashed dividends by 50% in 2022. Yield-chasers lost 30%+ of their capital overnight.

Procter & Gamble (PG): Boring? Sure. But they’ve raised dividends for 68 years straight, including during 2008’s meltdown.

Hunt for dividend durability instead:

15+ Years of Dividend Growth (not 10—too many impostors sneak in).

Earnings Growth > Inflation + 2% (if inflation’s 3%, demand 5%+).

Payout Ratio < 50% (forget 60%—go safer).

Example:

Lowe’s (LOW): 50-year dividend growth. Payout at 35%. Earnings up 12%/year. That’s fortress-level.

Mistake #2: Ignoring Total Return

I’ll say it plainly: Dividends alone won’t save you from inflation.

If your portfolio doesn’t grow, you’ll lose purchasing power.

Imagine two investors:

Investor A: 100% in high-yield stocks (6% yield, 0% growth).

Investor B: 100% in dividend growers (3% yield, 8% growth).

After 20 years:

Investor A’s $1M portfolio throws off $60K/year… but inflation-adjusted, it’s worth $27K in today’s dollars.

Investor B’s portfolio grows to $4.6M, throwing off $138K/year — with dividends that also grew 8% annually.

REINVEST DIVIDENDS RELENTLESSLY UNTIL RETIREMENT.

DRIP Everything: Automatically reinvest dividends into more shares. SCHD does this beautifully—its 3.5% yield + 10% annual growth turns $10K into about $26K in 10 years.

Hold Growth Compounders Early: Even in a dividend portfolio, allocate 20-30% to stocks like Microsoft (MSFT) or Apple (AAPL). They’re dividend payers now, but their share price growth will turbocharge your reinvestment.

Shift to Income 5 Years Out: Once you’re within 5 years of retirement, start redirecting dividends to cash. But until then, let compounding work.

BUT THERE’S A CATCH:

Pure dividend strategies can require $3M+ just to earn $100K/year.

That’s out of reach for most.

So how do you lock in income without a massive bankroll?

Simple: Combine dividends with surgical selling.

How Do You Extract Cash Without Killing Your Portfolio

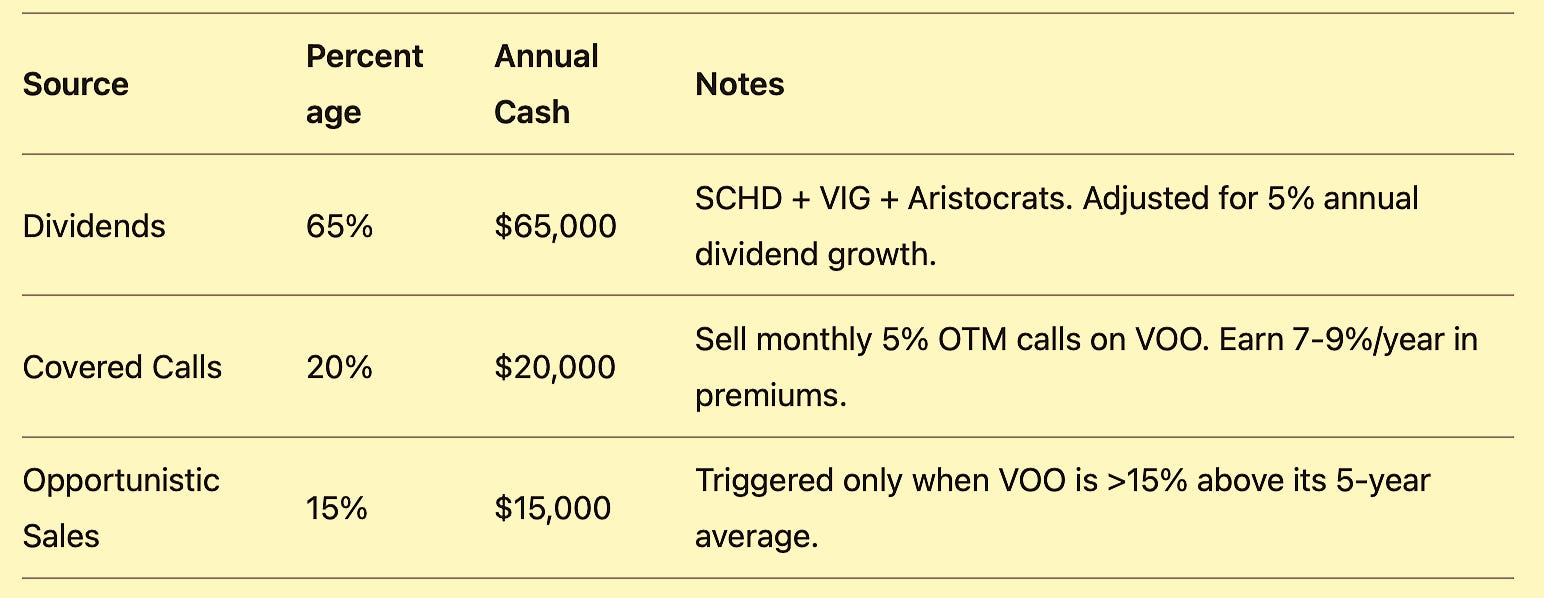

STEP 1: Build a Dividend Floor

Core Holdings (60% of portfolio):

SCHD: 3.5% yield, 10%+ annual dividend growth.

VIG: Lower yield (2%), but faster dividend growth (12%+).

Individual Aristocrats: 3-5 stocks like Lowe’s (LOW) or NextEra Energy (NEE).

This slice covers 60-70% of your income needs.

STEP 2: The "Opportunistic Selling" Fund (30%)

S&P 500 ETF (VOO): Sell calls against it. In bull markets, generate 5-8% extra yield.

Treasury Ladder: 3-month to 2-year T-bills. Roll maturing bonds into stock sales only when the S&P is >10% above its 200-day moving average.

Why This Works:

You’re selling high (bull markets) to avoid selling low (crashes). It combines safety (T-bills) with growth (S&P).

STEP 3: The "Oh Shit" Buffer (10%)

Cash + Gold + Long-Dated Bonds: Boring, but you’ll thank me when markets drop 30% and you’re not forced to liquidate.

The Withdrawal Blueprint: Exact Percentages, Exact Timing

Need $100K/year? Here’s the breakdown:

Keys to Success:

Never sell stocks when the Shiller P/E is> 30 (it’s 38 today, so no selling now).

Reinvest surplus dividends in downturns. In 2022, I plowed $20K of excess dividends into T-bills yielding 4%.

But even the best plan collapses if you sabotage yourself…

I’ve coached 500+ investors. And the #1 failure point? Psychology.

Trap #1: “This Time is Different”

When everyone’s buying AI stocks yielding 0%, you’ll itch to ditch dividends.

Don’t.

What to do instead?

Automate everything. Schedule your buys, sells, and rebalances each quarter. No spur-of-the-moment trades.

Keep a “Why” folder—pictures of your family, your dream home—so you remember what you’re really investing for when FOMO strikes.

You May Have Missed:

Yes, This Isn’t Sexy… And That’s Why It Works

No TikTok influencer will hype this. No CNBC guru will call you a genius. But while they’re chasing headlines, you’ll be sipping coffee, watching your dividends hit, and knowing your grandkids’ futures are set.

The system works if you do two things:

Stay disciplined.

Never compromise on the 15-year dividend rule.

The market rewards systems—not gambling. Build your system—and take what’s yours.

- Mike

This is probably the last time you can lock in Lifetime Access for only $199 → LINK

A 2023 survey by the National Financial Educators Council found that investing mistakes cost Americans over $388 billion (about $1,500 per person on average).

Poor investment choices can lead to setbacks, missed opportunities, and heightened risk—jeopardizing your financial security and retirement.

Chances are, you could be losing money in ways you don’t even realize.

That's why I offer exclusive, clear-cut investing strategies, in-depth market analysis, and carefully selected stock portfolios—delivered straight to your inbox every week—so you can make informed decisions and keep more of your money working for you.

Have a look at one of my premium weekly articles for free.

Trusted by over 52,000 investors across the US, with 710,000 monthly reads.

30‐day, risk-free, 100% money‐back guarantee.

Don’t wait for losses to pile up. Click below to subscribe and start taking control of your financial future today. The decision is entirely yours.