How Do I Start Trading Options? — Answering 5 Most Common Questions

After my post about subscribers making $7,104 in just two weeks from covered calls, my inbox exploded.

The most common message: "I've never traded an option in my life. How do I start?"

First, my 4-Bucket system forms the foundation:

Dividend Growth (aristocrats like JNJ),

High Yield (REITs, BDCs),

Value Hunt (quality on sale) and

Options Income (extract cash from shares via calls and puts).

But what transforms this from good to exceptional? — The options strategies that supercharge each bucket, potentially turning a modest 3-4% yield into 15%+ annual income without excessive risk.

Click here to learn about my proven approach to income investing

If you've been watching from the sidelines, feeling confused, I wrote this post specifically to clear things up.

But first, let me address the #1 question from these options newcomers:

"How exactly does the Multiplier snowball work if I've never traded an option in my life?"

The Multiplier snowball is beautifully simple:

Collect option premium → Cash drops into your account TODAY

Buy more shares with that cash → Your next dividend checks get bigger

Sell options on the new shares → You pocket even more premium

Repeat → Each round stacks on the last—small at first, huge later

This looks trivial in the beginning. Your first month's premiums might buy just 4 extra shares. But those 4 become 6, then 10, then 20 as the loop repeats.

By year three, what started as a trickle becomes a flood of monthly income.

Now let's tackle the other burning questions:

Question #1: "Cut the jargon—what EXACTLY happens when I sell a covered call on my dividend stock?"

The financial industry loves making simple concepts sound complicated.

Here's the plain truth:

You own 100 shares of Johnson & Johnson at $152.

You sell someone a "lottery ticket" that pays them if JNJ goes above $160 in the next 40 days.

They pay you $210 right now for this ticket.

That's it.

That $210 hits your account TODAY. Not in 40 days. TODAY.

Then one of two things happens:

JNJ stays below $160: You keep your shares AND the $210. Sell another ticket next month.

JNJ goes above $160: You sell your shares at $160 (making $8/share profit) AND keep the $210.

Either way, you win.

And yes, you still collect the dividend while waiting.

Now multiply this by 5-10 positions in your portfolio, and you're looking at an extra $1,000+ monthly income from stocks you were going to hold anyway.

The real-world numbers:

And these aren't cherry-picked results:

→ Last Thursday's cash-secured puts are already up +2.7% in just seven days - While most dividend strategies deliver around 0.75-1% quarterly, my picks generated nearly three times that in a single week.

→ My subs collected $7,104 in covered-call income over 14 days - On roughly $190k of stock, triple the S&P's return in two weeks flat.

Question #2: "How much do I really need to get started with options? Everyone gives different answers."

Let me end the confusion:

You need $25,000 minimum to start implementing this properly.

Why $25,000 and not the $2,000-5,000 that Reddit keyboard warriors suggest?

Because:

You need to control at least one 100-share lot of QUALITY companies (not penny stocks)

Most decent dividend payers cost $50-150 per share ($5,000-15,000 per 100 shares)

You need multiple positions to generate meaningful income

Could you start with less?

Sure, just like you could start a construction business with a hammer and a screwdriver.

But you'd be severely limited.

My blunt advice: If you have under $25,000 to invest, focus on building your capital base first. The Multiplier system works dramatically better at $50,000+, and becomes a retirement game-changer at $250,000+.

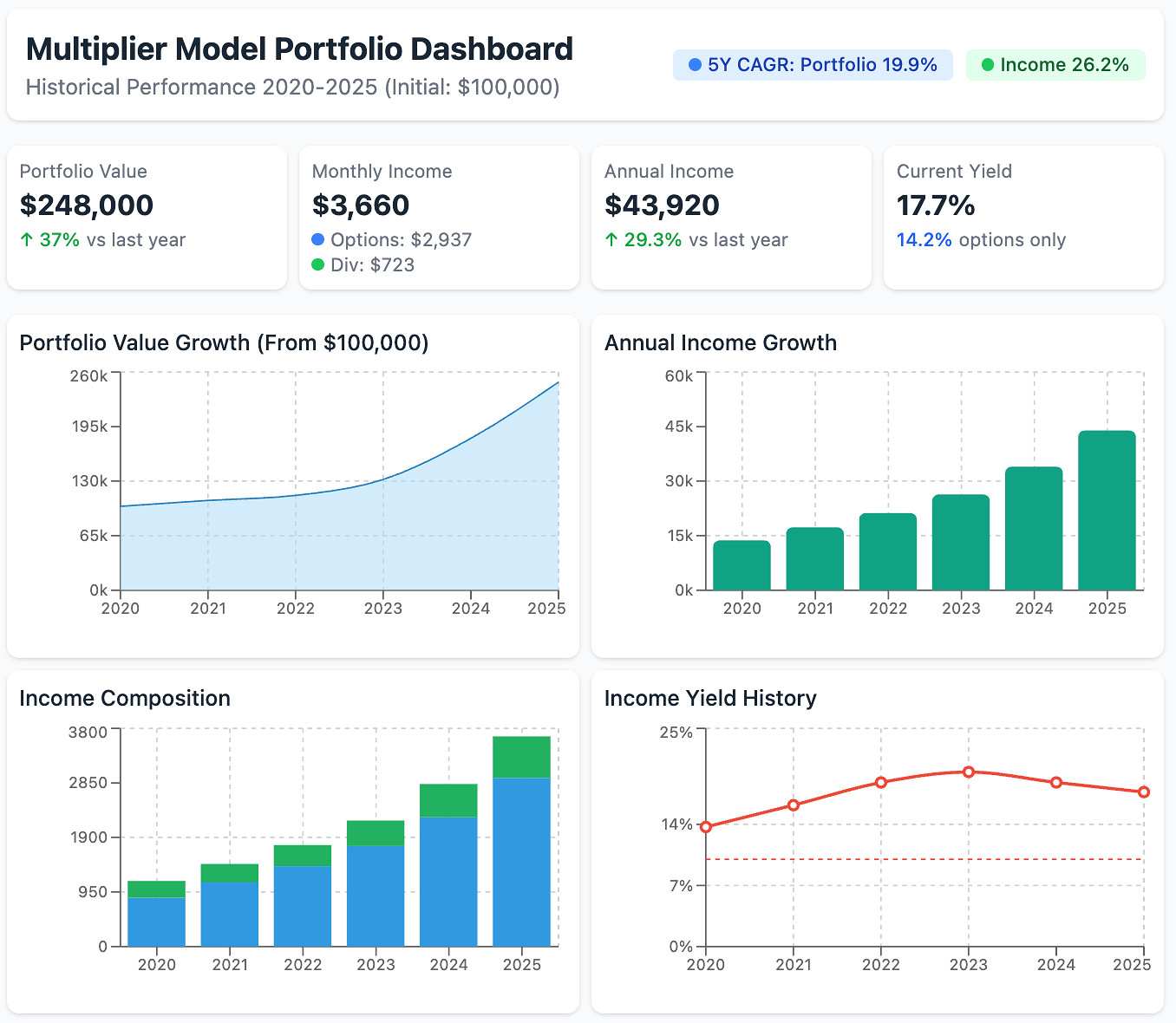

My Multiplier model portfolio started with $100,000 in 2022 and now generates $3,660 monthly in dividends + options premiums.

That's $43,920 annually from a six-figure portfolio.

Scale that to $500,000 and you're looking at $22,750 monthly.

That's life-changing income.

Question #3: "What happens when my stock gets called away? Doesn't that ruin The Multiplier approach?"

This question reveals how thoroughly Wall Street has brainwashed average investors.

Getting your shares called away isn't a failure—it's a win.

You made the maximum possible profit on that position!

Let's be crystal clear with an actual example from last month:

Owned 100 shares of Cisco (CSCO) at $47.83.

Sold the $52.50 call for $1.15 ($115 premium).

CSCO rose above $52.50, and the shares got called away.

Here's the actual profit breakdown:

Share appreciation: $52.50 - $47.83 = $4.67 per share ($467 total)

Option premium: $115

Total profit: $582 on a $4,783 investment in 38 days (12.2% annualized)

But here's where the Multiplier magic happens:

The very next day, I sold a $50 cash-secured put for $1.35 ($135 premium).

This does two things:

Generates ANOTHER immediate income payment

Potentially lets us buy CSCO back at $50 (still above our original cost but below what we sold for)

This call-put cycle can continue indefinitely, generating income regardless of market direction.

Last year, I ran this exact cycle on Pfizer (PFE) four times, generating $862 in premiums on a ~$4,000 position.

That's an extra 21.5% yield on top of the dividend.

Question #4: "How do I know which options to sell? There are too many strikes and dates!"

This is precisely why I share VADER with my premium subscribers (the Volatility Arbitrage Dividend Enhancement Return algorithm from my trading desk days).

VADER does the heavy lifting for you by:

Scanning 3,217 optionable stocks nightly

Filtering them through 16 specific criteria, including liquidity thresholds, volatility patterns, and technical support levels

Eliminating risky candidates with weak balance sheets, thin trading, or surprise earnings

Scoring what remains on both safety and premium potential

Delivering ready-to-trade lists organized by risk tolerance

The result — three simple lists delivered twice weekly:

🔒 Conservative (80-85% probability of success, lower premium)

⚖️ Balanced (70-75% probability, medium premium)

🔥 Aggressive (60-65% probability, higher premium)

You can easily tailor it to YOUR comfort level.

Check this free-for-all post to see how it looks for the premium subs:

For those without VADER access, focus on these three factors:

Delta between 0.20-0.30

This gives you approximately 70-80% probability of keeping your shares.30-45 days until expiration

This sweet spot maximizes premium per day while giving enough time decay.Strike price above your cost basis

Never, ever sell calls below what you paid for the stock.

The beauty of VADER is that it handles all the complex calculations and screening while you focus on selecting what works best for your specific portfolio and risk tolerance.

New VADER covered call selections drop tomorrow for all Premium subscribers.

Question #5: "Will this strategy survive a market crash? I'm worried about another 2008 or 2020."

This question reveals who actually lived through 2008 versus who just read about it.

Options income strategies like covered calls and cash-secured puts have OUTPERFORMED during every major market correction over the past 25 years.

Look at the actual numbers:

2008 Financial Crisis: S&P 500 (-37%) vs. BXM (-28%)

2020 COVID Crash: S&P 500 (-33.9%) vs. BXM (-28.5%)

2022 Inflation Bear: S&P 500 (-18.1%) vs. BXM (-11.4%)

That's historical fact.

Why do options income strategies hold up better?

Two reasons:

The premium you collect acts as a downside buffer

Volatility spikes during crashes, which means BIGGER premiums

During the March 2020 COVID crash, option premiums on blue-chip stocks nearly tripled.

While everyone else was panicking, Multiplier practitioners were collecting their biggest paychecks of the year.

The financial media benefits from our fear.

"What's the Multiplier snowball effect and how does it really work?"

The Multiplier snowball effect is mathematically simple but psychologically difficult for most investors to maintain:

Collect dividend + option income

Reinvest 25% of that income to buy more shares

Those additional shares generate both more dividends AND more options premium

Repeat until your income exceeds your expenses

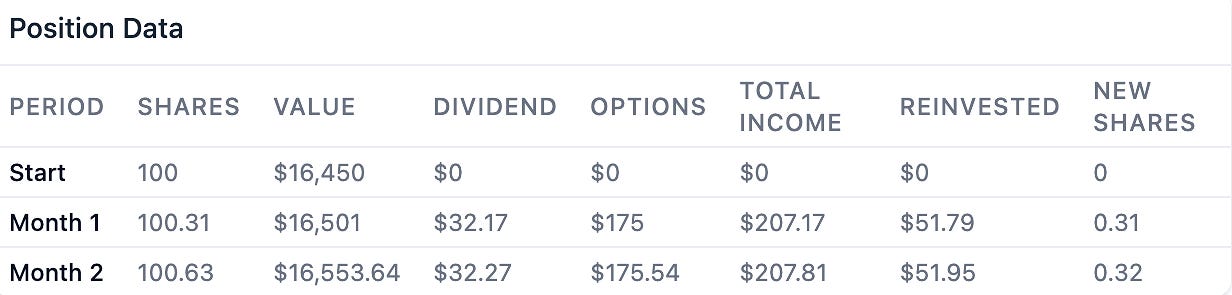

Let me show you the numbers from my model portfolio:

Starting point: 100 shares of Procter & Gamble (PG) at $164.50

Month 1:

Dividend: $96.50 quarterly ($32.17 monthly)

Options premium: $175 monthly

Total monthly income: $207.17

25% reinvested: $51.79 (adds 0.31 shares)

Month 2:

Now own 100.31 shares

Dividend: $32.27 monthly

Options premium: $175.54 monthly

Total monthly income: $207.81

25% reinvested: $51.95 (adds 0.32 more shares)

This looks trivial at first—adding fractions of shares.

But compound this over 24-36 months, and the growth becomes significant.

By year 3, that same initial position typically generates 40-50% more income than it did in year 1, with minimal additional risk.

Wall Street has convinced millions that generating meaningful retirement income requires either taking enormous risks or having multi-million-dollar portfolios.

This narrative is demonstrably false.

My Multiplier system isn't revolutionary—it's the same approach institutions and wealth management firms have quietly used for decades.

I hope today's fundamentals bring you one step closer to the retirement income you deserve.

I'll be back tomorrow with the best covered calls from VADER for the premium subscribers.

Thank you for tuning in today and supporting my work!

Mike Thornton, Ph.D.

What is the rationale for only using 25% of the proceeds to buy more shares?

Great explanation. I jumped into this concept in 2020 while WFH. I had good results but didn’t understand its true value.

What are your rules on buying back the sold calls or puts? Buy back if you hit 50%? Roll up or down with the same expiration date? Just let them expire?