Buffett’s Valuation Framework #2: Pick The Right Stocks In 2025

Lesson 2 in my Valuation Series: Turn Guesswork into Confident, Profitable Investing

I’ve been in the trenches of investing long enough to watch flawless models get ripped to shreds by the next morning’s news cycle. You can burn the midnight oil running all your numbers, only to have some surprise CEO scandal blow it all up by lunchtime.

That’s the reality of valuation: the market doesn’t care about your spreadsheets, and it sure as hell doesn’t care about your comfort zone.

If you’re about hitting financial independence and picking winning stocks, you’ve got to stop wishing for perfect clarity and start thriving on these twists.

This is the second free masterclass in my series, designed to elevate your investing skills and put you in control. It’s filled with actionable insights to help you build a rock-solid foundation for evaluating businesses—no reliance on online gurus, no hype-driven stock picks, just proven strategies.

If you missed the first one:

In this lesson, I want to eliminate all unnecessary details—no fabricated synergy nonsense, no elaborate formulas that obscure common sense. I’ll show you exactly how I evaluate companies, why I do it my way, and how you can immediately apply it to your own portfolio.

If that sounds like your kind of game, let’s dive in.

I’ve had plenty of people come to me thinking, “Hey, once I’ve worked the numbers, I’m done.” Let me shatter that illusion: the second your valuation is complete, it’s already obsolete. Corporate boards vote on unexpected mergers, CEOs quit, lawsuits drop from the sky, or some macro bombshell spooks the market. That’s the game. You do your best with the info you’ve got, and then you move on.

Stop beating yourself up if the world changes after your analysis. You can’t push “pause” on reality.

Three Ways to Put a Number on a Company

When I first started investing, I thought there was one “right way” to do valuations. I was dead wrong. There are three main approaches, each with its own quirks:

Intrinsic Valuation (a.k.a. Discounted Cash Flow)

You look at expected cash flows, growth, and risk—then discount it all back to the present. You’re laser-focused on the company’s fundamentals, ignoring Wall Street’s mood swings.Pricing (a.k.a. Comparable Analysis)

You check what “similar” companies trade for and slap a multiple on your target. It’s basically, “How does the market price others in the same sector? Let’s piggyback on that.”Contingent Claim/Option-Based Valuation

Useful for lottery-ticket companies: early-stage biotech with one drug in the pipeline, oil explorers sitting on potentially worthless reserves—stuff that might be worth zero or a fortune depending on a specific event.

You can run all three and get four different answers (yes, four, because option valuation usually layers on top of an intrinsic model).

Then you face the real-world decision: buy, sell, or hold? No weasel words like “slightly bullish” or “moderate underperform.” Make the call.

Bias Is Everywhere—Stay Honest

Everyone who values a company has an agenda. If you’re doing it for your own portfolio, maybe you already love the CEO or hate the brand. If you’re working for a big bank, your boss might nudge you toward a certain number so the pitch deck “flows” nicely. If you’re at a startup, you want that sky-high figure so venture capitalists give you easy money. It’s all bias.

When you love a stock, you magically crank up growth rates and downplay risks.

When you hate a stock, you nudge margins lower and push the discount rate higher.

Don’t even try to pretend you’re 100% objective. Instead, acknowledge your bias. It’s the only shot you have at not letting it ruin your analysis.

Intrinsic Valuation: Fewer Friends, More Depth

Pros

Serious Deep-Dive: You’re forced to understand the guts of the business—products, expansion plans, cost structure, strategic advantages.

Long-Haul Focus: When you’re in it for five, ten years, you’re not panicking if the stock dips 10% next quarter.

Cons

Time-Consuming: Gathering numbers, building a real model, and studying the business is a grind.

Unpopular: Everyone is talking about the next hype name. You’ll look like an outlier when you pass on it based on cold hard cash-flow projections.

If you’ve got the stomach to be a contrarian and enough patience not to bail out at every bump, intrinsic valuation can be your edge. But it’s not a quick-flip or momentum-chasing strategy.

Additional Practical Tip:

When running a discounted cash flow (DCF), I pick a discount rate by starting with the “risk-free rate” (often the 10-year U.S. Treasury yield) and then adding a market risk premium (historically 4–6%, though it can shift if the market’s ultra-volatile). If the stock is riskier (small-cap, shaky balance sheet, or cyclical sector), I throw in another risk premium on top to reflect the possibility that cash flows might not pan out.For estimating growth rates, I usually look at historical revenue growth, factor in macro tailwinds or headwinds, and—if the company’s young—scan how peers in that growth phase performed in their early years. I never trust management’s guidance blindly. I’ll check analyst projections, but I apply some skepticism to keep it real.

Pricing: Strength in Numbers (Maybe)

Pros

Fast & Dirty: Pull a few multiples off competitor stocks, do a quick ratio, and boom—you have a “fair price.”

Synchronized with the Market: If the sector is trending, you can ride that wave more easily.

Cons

Sector Bubbles: If every stock in an industry is trading at insane valuations, your “fair price” might be equally insane. So you’re basically relying on the crowd not to be a flock of sheep heading off a cliff.

Less Insight: You might miss serious weaknesses or strengths that the herd hasn’t spotted yet.

Pricing can be gold if your time horizon is short, or if your job demands sector allocation no matter how frothy the valuations get.

Additional Practical Tip:

When doing comparable analysis, I like to keep a “stress test multiple” in my back pocket. For instance, if the sector average P/E is 25, I’ll run the valuation at 20 and 15 too, just to see how the stock holds up if the market stops being so generous. If the investment still looks good at a more conservative multiple, that’s a green light. If it only works out at nosebleed valuations, I steer clear.

The Option Angle: When There’s a Binary Outcome

You might come across a company that’s not generating steady revenue but is pinning its hopes on a single big project. Could be a new drug, a high-risk technology, or untapped natural resources. In that scenario, a standard DCF can look ridiculous—the present value might come out to peanuts because the near-term cash flow is nonexistent.

Option-based methods try to factor in the probability of success and the payoff if that success materializes. It’s tricky, but ignoring this angle can lead you to totally miss the lottery ticket paydays.

A Quick Mini-Walkthrough (Hypothetical)

Say there’s a biotech with zero current revenue but a phase-2 drug that, if approved, could generate $500 million annually for five years. I might assess the probability of success at, for example, 30%. Then I’d discount the $500 million for five years back to the present and multiply by 0.30. If that final figure is comfortably above the current market cap, there’s potential. If not, I keep my powder dry.

M&A and the Magic of “Synergy”

If you’ve ever wondered why bankers conjure up synergy in almost every takeover deal, here’s the raw truth: it’s the fudge factor. The buyer says, “We’re only paying $X because we’ll get these massive synergy benefits.” The seller counters, “We’re worth at least $Y because we deliver synergy to the acquirer’s operations.” Both sides wave synergy around to justify valuations that might otherwise never align.

I’ve been in countless M&A rooms where synergy was the mystical unicorn that supposedly made everyone a winner—especially the bankers collecting huge fees. Don’t get suckered by synergy unless you can map out exactly where those extra revenues or cost savings will come from. If it’s not spelled out, it’s probably just a sales pitch.

Concrete Synergy Example for a Mid-Cap

Let’s say a mid-cap widget manufacturer acquires a smaller competitor that has a big presence in a neighboring state. If the acquirer can integrate the competitor’s logistics network seamlessly, they might see cost savings on shipping—maybe to the tune of $5 million a year. That’s real synergy if you can validate the shipping costs, route overlaps, or distribution expansions. But if all you hear is “Cross-selling opportunities” with zero specifics, run your own numbers (or just walk away).

My No-Nonsense Approach to the “Project”

In the spirit of teaching you to fish instead of just handing you a plate of sushi, I’m challenging you to roll up your sleeves and apply all these methods—intrinsic valuation, pricing, and (if applicable) option-based—to a company you find compelling. Don’t pick something “easy” just because it has a century of stable earnings. Stretch yourself:

Look at a firm that’s losing money but has big growth potential.

Consider a non-US stock to get outside your comfort zone.

Dive into a company with a service-based model—they’re often less transparent than old-school manufacturing.

By the time you do a discounted cash flow analysis, then compare that with a pricing multiple, and maybe sprinkle in an option-based tweak, you’ll likely end up with more than one number. Awesome. That’s normal. Now you have to decide: do you buy, or do you dump it? No halfway nonsense like “slight overweight.” Make the call.

Putting It into Practice for Early Retirement

I’ve had skeptical, FIRE-focused readers ask me, “Alright, so how does this help me retire early?” Let’s get tactical:

Pick One Core Method:

If your holding period is 5–10+ years, lean into intrinsic valuation so you can see if the business’s future cash flows justify today’s price.Run a Pricing “Sanity Check”:

Compare the stock’s multiples to peers, but don’t let crowd frenzy blind you. If the entire sector is insanely priced, you might be inheriting a bubble.Set Explicit Triggers:

Maybe you’ll tolerate a 20% drop if you still believe in the thesis. Or you’ll sell if a new competitor destroys the company’s moat. Write these down before your emotions kick in.Revisit Your Valuation Quarterly or Semi-Annually:

You’re aiming for early retirement, so track how the story evolves. Revenue falling off a cliff? Margins contracting? Adjust your model accordingly.Map It to Your Retirement Timeline:

If you’re gunning for financial independence in a decade, you need to consider whether this stock will still be compounding over that entire horizon. Some high-flyers burn out quickly.

Portfolio Context for the FIRE Crowd:

I’m a big believer in having a core of stable, diversified assets—like low-cost index funds or broad ETFs—to serve as the foundation. Then I use individual stock picks (valued using these methods) to “move the needle” a bit more aggressively. This mix helps me sleep at night because I’m not betting my entire retirement on one or two picks.When you dabble in more volatile stocks, remember that overtrading can be a performance killer. Commissions may be low these days, but the real cost is emotional whiplash. I’ve found that it’s crucial to set a limit on how often I rebalance or switch positions—quarterly or semi-annually works fine for most. That discipline helps me avoid panic-driven decisions.

A Quick Real-Life Example (Hypothetical)

Let’s say you find a mid-cap utility that pays a moderate dividend and has stable, regulated revenue. You do a back-of-the-envelope DCF:

Forecast modest annual revenue growth (e.g., 3–4%) since it’s a steady utility.

Project a stable margin because utilities typically have regulated rates.

Discount back using a cost of capital that reflects relatively low risk (maybe 7–8%, accounting for the current 10-year Treasury yield plus a smaller risk premium).

Result: The intrinsic value might come out close to the current trading price.

Now check the Pricing angle: If peer utilities are trading at, say, 16x earnings and your pick is at 15x, maybe you’re getting a slight discount. Throw in a 3% dividend yield, and it could be a comfortable long-term hold. If your DCF is near the market price and you see no short-term catalysts to drop earnings, it might be exactly what you want in a FIRE-friendly, multi-year portfolio.

No drama, no day-trading nonsense—just a stable path toward compounding returns that help you get out of the rat race sooner.

Risk Management Note:

If the utility’s growth starts to stall or regulators start making noise about rate cuts, that’s a signal to revisit your assumptions. A once-stable pick can turn sour if political or environmental pressures pile up. Keep an eye on news, but don’t overreact to every blip.

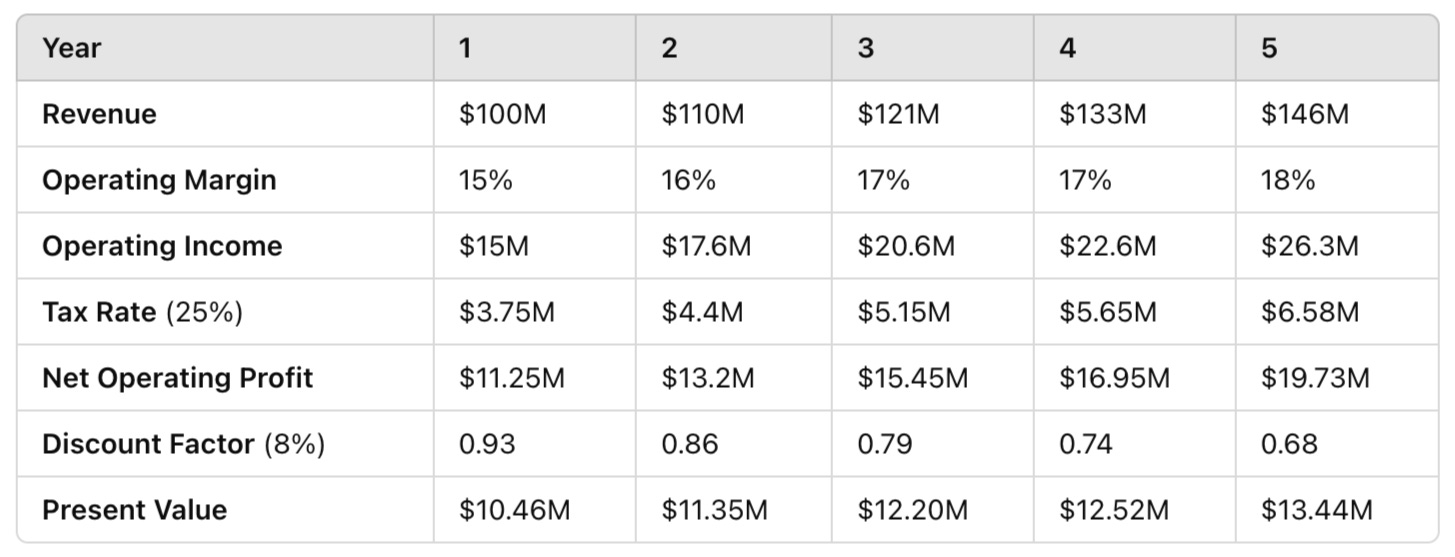

Additional Content: “Plug-and-Play” Valuation Example

Because I know some of you want an even clearer, more numerical framework, here’s a simplified snapshot of how I might build a basic DCF for a hypothetical company—call it “ACME, Inc.”:

Then, I sum up the present values of these five years—roughly $60.0M—and add a “terminal value” calculation for the period after Year 5 (for instance, using perpetuity or exit multiple approaches). Let’s say the terminal value, discounted back, adds another $90M. That yields an intrinsic valuation near $150M in total. If ACME, Inc. has a market cap of $120M, there might be an attractive margin of safety—assuming my assumptions hold water.

The point: you don’t need a 50-tab Excel monster. Even a quick table like this can give you a sanity check.

Additional Content: Broader Asset Allocation Nuances for investors focused on Early Retirement

I’m not just about stocks, either. If you’re dead serious about retiring early, you want multiple levers you can pull to smooth out returns and hedge risk. Let me expand:

Bonds or Fixed Income: In low-rate environments, bonds might feel unappealing, but they still provide ballast. If you have enough in government or high-quality corporate bonds, a market downturn won’t torpedo your entire portfolio.

Real Estate: Whether it’s REITs or direct property investment, real estate can deliver steady cash flow plus capital appreciation. If you’re comfortable managing tenants (or investing in a well-run REIT), real estate can diversify against stock market gyrations.

Cash Reserves: As you approach FIRE, you might want 1–2 years of living expenses in cash or near-cash instruments. This helps you avoid panic-selling stocks when the market dips and you still have bills to pay.

Index Funds or ETFs as a Core: This is my “bedrock.” Even if I’m analyzing individual companies, I like to keep a healthy chunk in broad market ETFs (like VTI for total U.S. market or VXUS for international exposure). It’s lower effort, lower stress, and historically outperforms a lot of individual pickers in the long run.

Risk-Return Alignment: Think of each asset class as a different “gear.” Stocks can skyrocket or crash, real estate is often steadier but illiquid, bonds generate lower returns but also lower volatility, and so forth. Pick your mix based on how soon you want to retire and how comfortable you are with short-term price swings.

The synergy of these components is what I lean on to ensure I’m not forced to liquidate good stocks at a bad time. If you’re all-in on a handful of momentum picks, a single bear market can set your early retirement plans back years. But with a multi-pronged portfolio, you can ride out storms more gracefully—and that’s what real financial independence is all about.

The Final Word: Action Is What Matters

Your spreadsheet can churn out 10 decimal points. Great. In the real world, nobody cares how many decimal points you used if you never put money on the table. You’ll forever be that person who’s “almost ready” while the market keeps barreling forward.

Here’s my bottom line:

Stop aiming for a perfect answer.

Own your bias, but don’t let it blind you.

Pick the valuation approach that fits your time horizon and temperament.

When it’s time to act, act.

And if the market flips the script tomorrow? You do your best to pivot. That’s life in the investment jungle. No whining, no do-overs, just the next decision on the horizon.

Thanks for sticking with me through this second lesson. Next time, we’ll rip apart a real-world case study or two. Keep pushing, keep hustling, and don’t forget: the market doesn’t wait for perfection.

One thing that's worked wonderfully for me is treating position sizing as an art form - starting small and building up as the investment thesis proves itself. Really adds another dimension to these solid valuation frameworks.

Hey Mike,

Did you continue this series on company valuations? Was a great read!