Buffett's Simple Strategy You Can Copy Right Now to Beat 90% of Investors and Retire MUCH Sooner

Trying to Time the Market? Just Stop

When I started investing, I thought I had an edge.

This wasn’t ego—I had the credentials, the tools, and the experience. I spent years in finance, analyzing markets, building predictive models, and breaking down corporate financials. My PhD was supposed to give me the inside track to spot trends and beat the market.

And for a while, it felt like I was winning. A well-timed trade here, a great stock pick there. But when I zoomed out and looked at my portfolio’s long-term performance, the truth was staring me in the face: I wasn’t outperforming the market consistently. Worse, the effort I was pouring in—research, time, stress—wasn’t worth the marginal gains.

That’s when I started to reexamine everything I thought I knew about investing. I wasn’t alone in failing to beat the market. In fact, almost nobody does. Even the ones running billion-dollar portfolios—can’t pull it off. That’s when I realized: Beating the market isn’t the goal. Owning it is.

I made plenty of mistakes trying to outsmart the market—mistakes that cost me time, money, and countless missed opportunities. That’s exactly why I’m writing this: so you don’t have to repeat them.

If I could start over today, I’d take a completely different approach. No hot stocks, no chasing trends, no unnecessary stress. Just what actually works.

I’d follow Buffett’s timeless advice: Own the market, minimize costs, and stay consistent.

I’ll show you the critical lessons I learned the hard way—and how you can skip the trial and error to focus on what delivers real results.

This article is exactly what I would do if I were starting today, knowing everything I know now. No wasted effort, no chasing distractions—just the strategies that actually work to build wealth smarter, faster, and with less stress.

Let’s dive in.

Section 1. The Odds Are Against You: Why Most Investors Fail

Let me be blunt: the market doesn’t care how hard you work.

It doesn’t reward effort or intelligence—it rewards discipline. That’s a brutal reality I had to face early in my investing journey. I was armed with a PhD in econometrics, years of experience in finance, and a belief that I could crack the code. I ran models, analyzed data, and fine-tuned my strategies to perfection. But the truth? The market humbled me.

And it’s not just me. Professional money managers—the ones with algorithms, insider access, and top-tier analysts—fail to beat the market consistently. Here’s why.

1. Active Management: A Losing Game

The numbers are staggering: 90% of actively managed U.S. equity funds underperform the S&P 500 over a 20-year period (SPIVA report).

Let that sink in—90%.

The chart above shows the percentage of large-cap U.S. equity funds underperforming the S&P 500 each year. Source: BetaShares SPIVA Report Analysis

So, why do they fail?

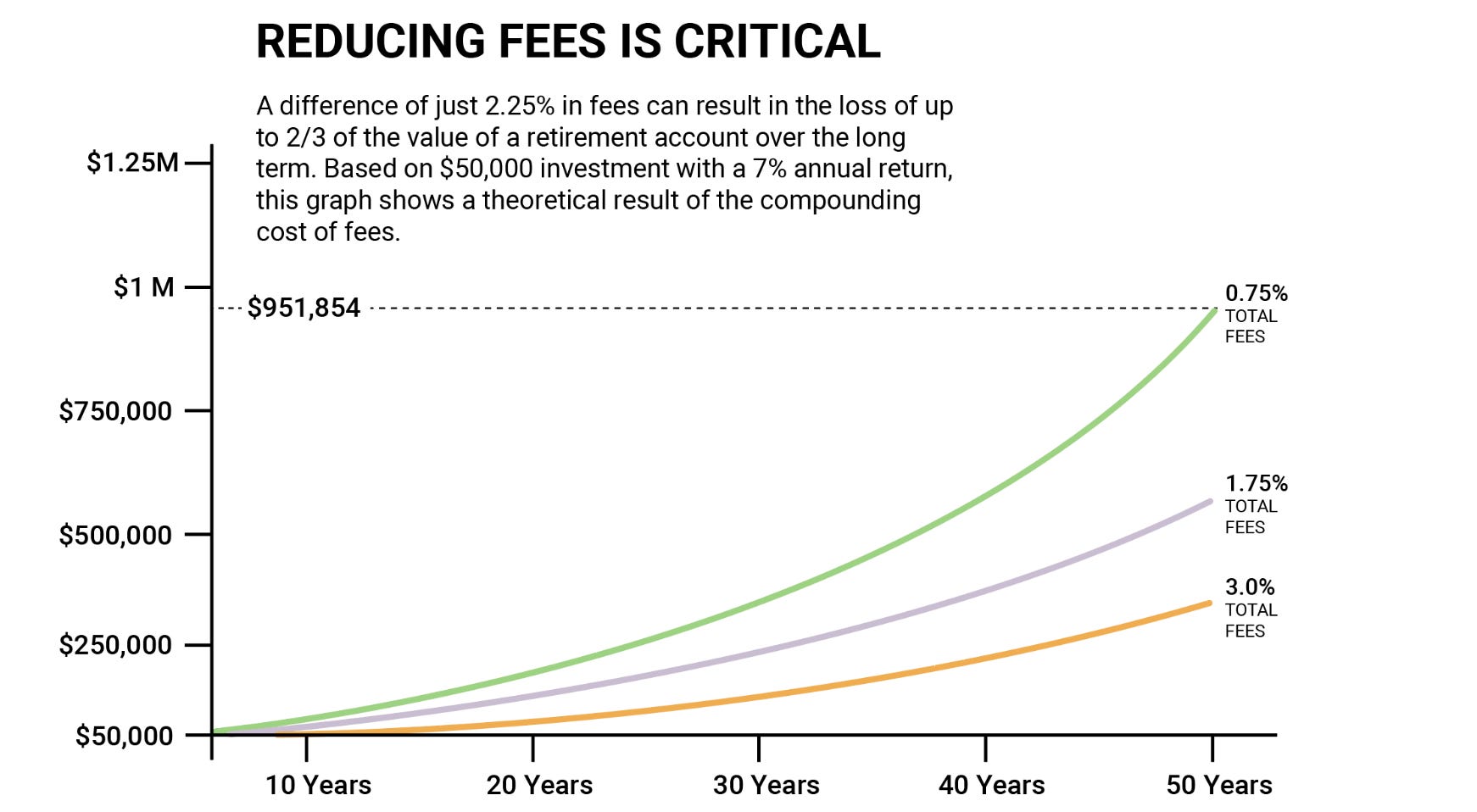

🔴 Fees Are a Silent Killer - Every active fund comes with fees—whether it’s a mutual fund charging an average 0.66% annually or a hedge fund taking 2% of your portfolio plus 20% of any profits. These fees may seem small, but over time, they destroy wealth. Compare that to an index fund like Vanguard’s S&P 500 ETF (VOO), which charges a microscopic 0.03%.

To put this into perspective, imagine a $100,000 investment growing at 7% annually over 30 years:

Without fees: $761,000.

With a 1% fee: $574,000. That’s $187,000—nearly 25% of your wealth—lost to fees. And that’s just the average mutual fund. Hedge fund fees are even more devastating.

Source: One Day in July - Low Fees Matter.

🔴 Frequent Trading Creates Drag

Active managers try to time the market, jumping in and out of positions to chase short-term gains. But every trade incurs costs: transaction fees, bid-ask spreads, and taxes. Over time, these constant losses eat into returns. Even worse, studies show that most active managers can’t time the market correctly anyway, turning what they think is a strategy into a handicap.

2. Taxes: The Silent Wealth Killer

A high-turnover mutual fund might generate annual taxable gains, forcing you to pay taxes on both short-term and long-term gains every single year. Those taxes don’t just reduce your returns—they also compound against you over time.

For example, if you’re in a 24% federal tax bracket, every $1,000 in realized gains costs you $240. Now multiply that by dozens of trades over decades. It adds up fast.

Index funds track the market and rarely trade securities, meaning they don’t generate taxable events. ETFs like Vanguard’s Total Stock Market Fund (VTI) take it a step further by using an “in-kind redemption” process to avoid triggering capital gains. This allows your money to stay invested and compound tax-deferred.

A high-turnover fund might cost you tens or even hundreds of thousands of dollars in unnecessary taxes over 30 years. Index funds? Virtually none.

3. Market Timing: A Fool’s Errand

If you’ve ever thought you could time the market, let me save you years of frustration: you can’t. Nobody can—not me, not Warren Buffett, not the most sophisticated hedge fund. And if you’re trying, you’re probably doing more harm than good.

The Market Moves Fast

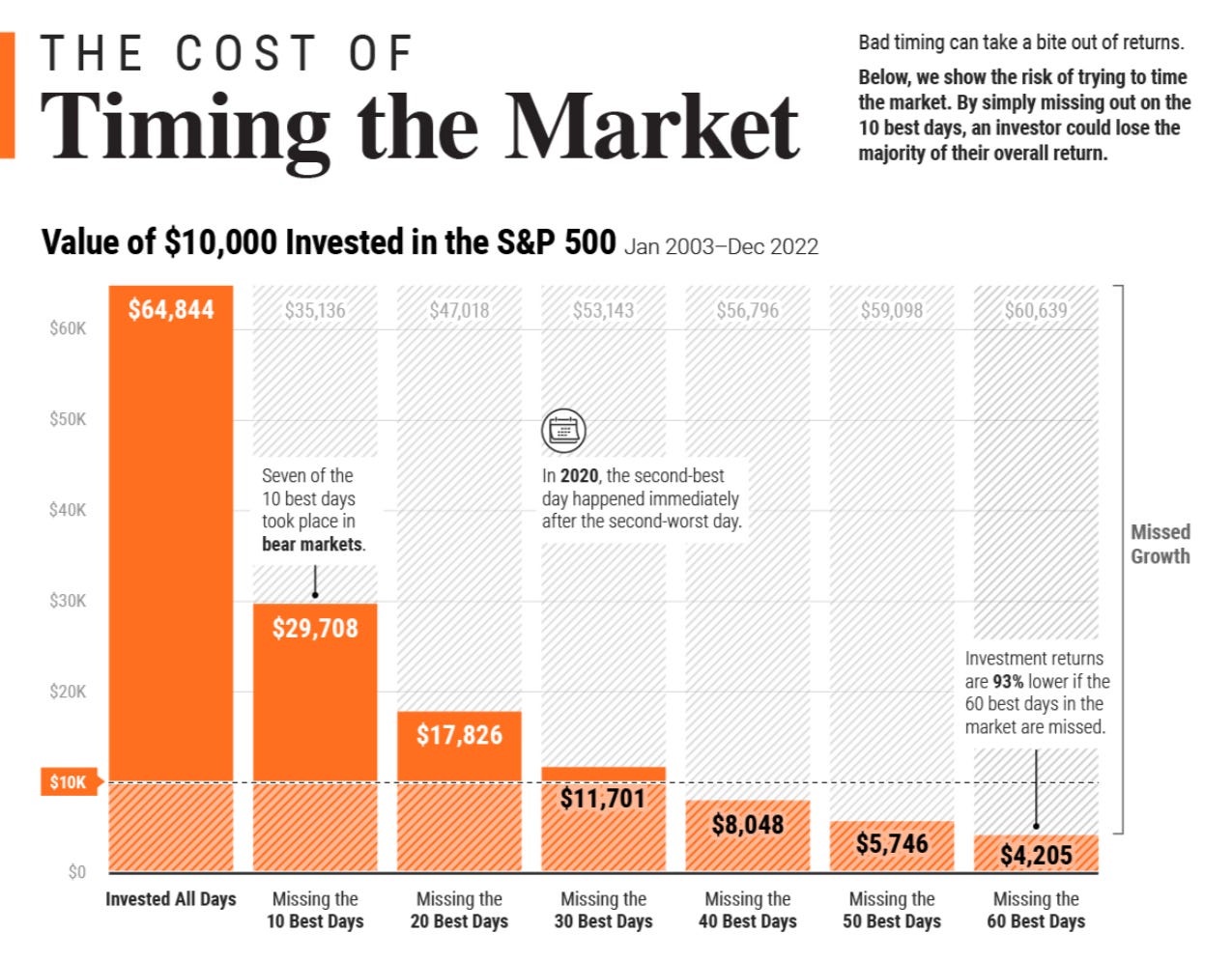

A study by JPMorgan found that 7 of the best market days over 20 years occurred within two weeks of the worst days. If you panic-sell during a downturn, you’re almost guaranteed to miss the recovery. Missing just the 10 best days in the market can cut your returns in half. For example:

A $10,000 investment in the S&P 500 from 2002 to 2022 grows to $61,685 if fully invested.

Miss the 10 best days, and that same $10,000 only grows to $28,260. That’s the price of market timing gone wrong.

Source: Visual Capitalist

Human Emotion is the Enemy

Fear and greed are the two emotions that drive most investors’ decisions—and they’re almost always wrong. When markets crash, fear takes over, and the instinct is to sell. By the time you feel comfortable re-entering, the market has already rebounded. This cycle of panic-selling and chasing returns locks in losses and forfeits gains.

Index funds eliminate this emotional rollercoaster. They stay invested through the ups and downs, allowing you to capture the market’s long-term growth without the destructive behavior that plagues most investors.

Section 2. Buffett’s Bet: Why Index Funds Win

In 2008, Warren Buffett made a wager that sent shockwaves through the financial world.

He bet $1 million that a simple, low-cost S&P 500 index fund could outperform a hand-picked portfolio of hedge funds over the next 10 years. Think about what he was up against: elite hedge fund managers armed with state-of-the-art technology, insider access, and the sharpest financial minds in the business. These were the best of the best, the so-called “smart money.”

On the other side? A no-frills, low-cost index fund. No flashy strategies. No algorithms. Just a simple fund designed to mirror the performance of the U.S. stock market.

The result wasn’t just surprising—it was a wake-up call. The index fund trounced the hedge funds, delivering an annualized return of 7.1%, while the hedge funds eked out a pathetic 2.2%. Over 10 years, that’s not just a small difference—it’s a staggering gulf in performance.

Why Did the Hedge Funds Lose?

Hedge funds lose not because they’re run by incompetent people—they’re not. Many of these managers are brilliant. They lose because the very structure of their business works against long-term success.

Here are the two key reasons Buffett’s index fund won—and why most investors are better off following his example:

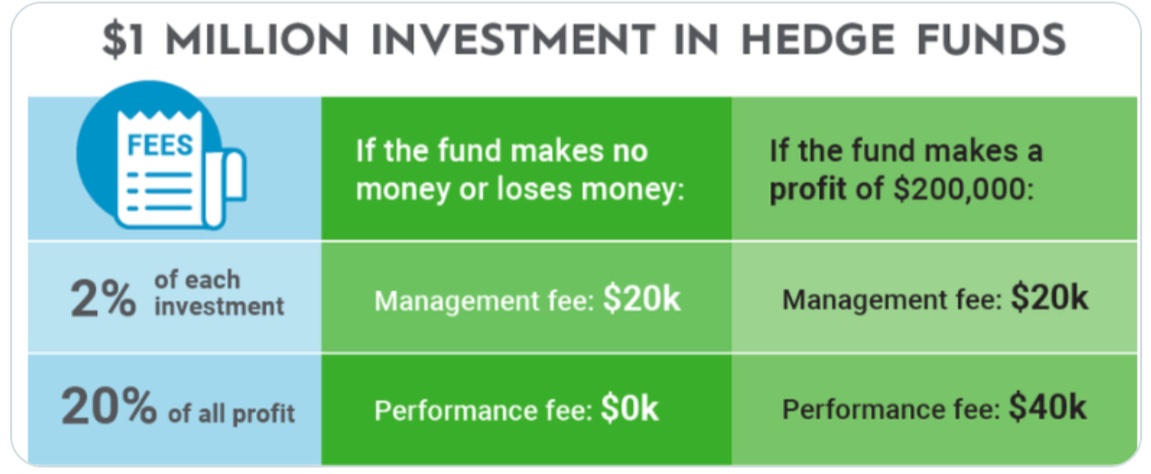

1. High Fees:

Hedge funds operate on what’s known as the “2 and 20” model. They charge 2% of assets annually and take 20% of any profits. At first glance, that might not sound so bad—if they’re delivering stellar returns, who cares? But here’s the catch: in most years, they don’t.

Source: Twitter

Let’s break this down with some simple math. Say the market delivers a 10% annual return (which is historically average for the S&P 500). A hedge fund matching that performance would still leave its investors with only 4-5% returns after fees. Why?

2% gets shaved off the top immediately.

20% of the remaining profits are taken as well.

Over time, this fee structure becomes an insurmountable drag on returns.

I’ve worked with clients who were enamored with the idea of hedge funds—until they saw the numbers. One client in particular had $500,000 in a hedge fund that returned 8% in a good year. After fees, they were left with less than 5%.

Had they put that money into an S&P 500 index fund with an expense ratio of 0.03%, their returns would have been almost double. And that’s before factoring in taxes (more on that later).

2. Short-Term Thinking: The Achilles’ Heel of Hedge Funds

Hedge fund managers are under constant pressure to deliver quarterly gains. If they don’t, they risk losing investors—or worse, being shut down altogether.

This pressure leads to two destructive behaviors:

🔴 Frequent Trading

Hedge funds often trade in and out of positions rapidly, chasing short-term opportunities. This approach:

Racks up transaction costs: Every trade incurs fees, spreads, and commissions.

Increases the likelihood of costly mistakes: The market is unpredictable in the short term, and even the best managers can’t consistently make the right call.

🔴 Failure to Ride Out Volatility

Long-term investing requires patience—something hedge funds can’t afford. When markets dip, hedge funds often sell to avoid reporting losses, even if holding would have led to long-term gains.

By contrast, index funds are immune to this noise. They ride out the ups and downs, allowing compounding to work its magic over time.

Source: ETF Trends

Section 3: Why Index Funds Work for Early Retirement Goals

If you’re pursuing Financial Independence, Retire Early (FIRE), index funds are the ultimate wealth-building tool. FIRE is all about maximizing savings, minimizing costs, and letting compounding do the heavy lifting.

1. Predictable Compounding

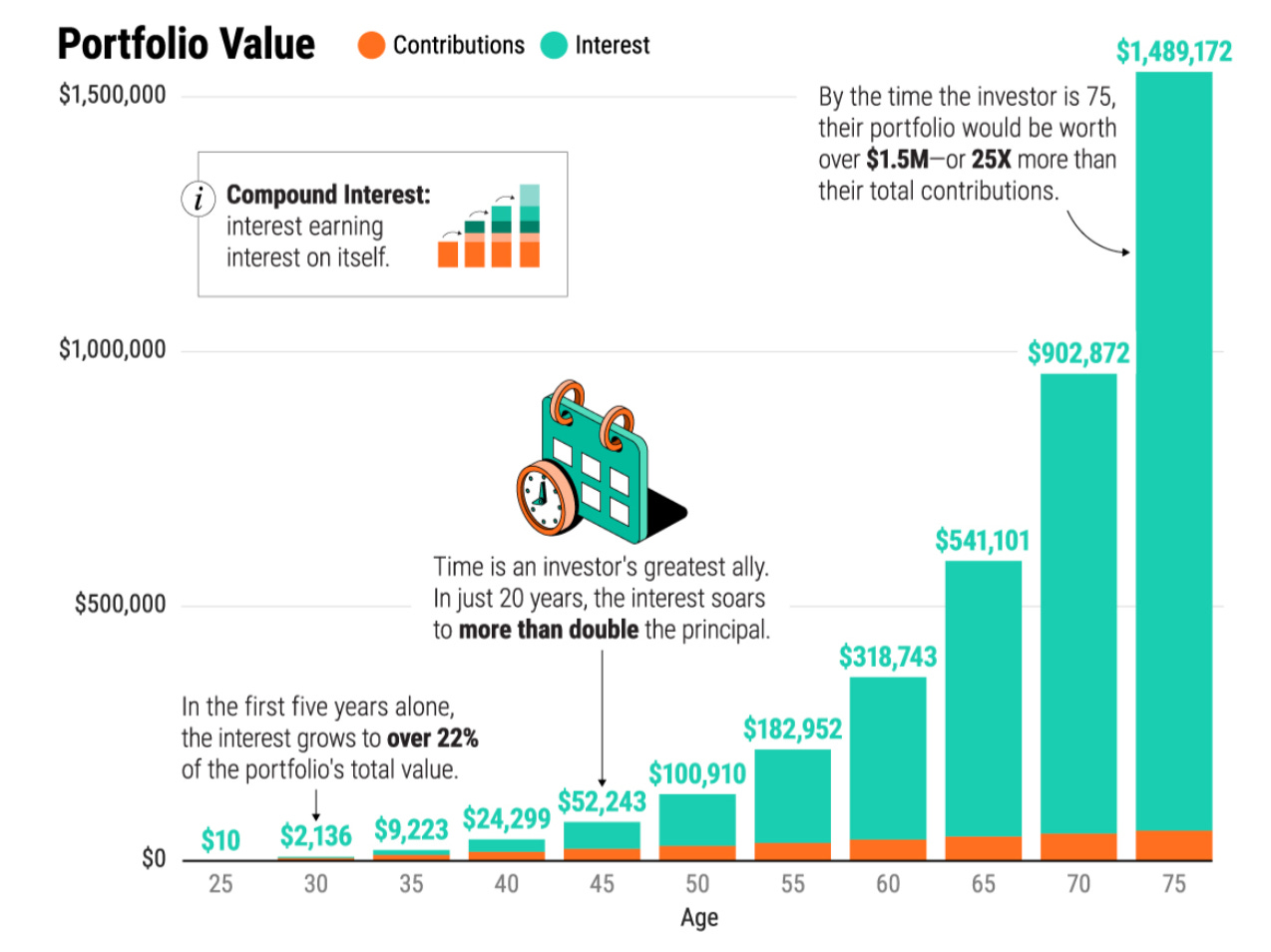

The S&P 500 has delivered an average annual return of 10% since 1926, or 7% after inflation. Despite crashes and bear markets, the long-term trend is overwhelmingly positive.

Invest $1,000/month starting at age 25, and by 50, you’ll have $1.2 million.

Start at 30, and you’ll still have $850,000 by 50.

Source: Visual Capitalist

The takeaway? Time in the market beats timing the market.

2. Automation Simplifies Success

Set up automatic contributions to accounts like 401(k)s, Roth IRAs, and HSAs. Automation removes emotions from the equation, ensuring you keep investing consistently—even during market downturns.

3. Tax Efficiency

Index funds are inherently tax-efficient, with low turnover and minimal taxable events. Combine this with FIRE strategies like Roth conversion ladders and HSAs, and you’ll grow your wealth while keeping Uncle Sam out of your pocket.

The Drawbacks of Index Funds

Index funds are powerful, but they’re not without flaws. Here are the key drawbacks—and how to address them:

1. Market Volatility

Index funds rise and fall with the market. During downturns, this can be painful—especially for retirees withdrawing funds during a bear market, which could lead to sequence-of-returns risk.

🔑 Solution: Use a bucket strategy. Keep 3-5 years of living expenses in cash or bonds to cover short-term needs while letting the rest of your portfolio recover.

2. No Outperformance

Index funds match the market. For most investors, this is ideal, but if you have the skill, time, and discipline (and let’s be honest, most don’t), you might achieve better results with niche strategies.

🔑 Solution: Consider allocating 10-15% of your portfolio to factor-based funds targeting “value,” “momentum,” or other proven factors.

3. Concentration Risk

The S&P 500 is heavily weighted toward large tech companies like Apple, Microsoft, and Amazon. If tech struggles, your portfolio might feel the hit disproportionately.

Source: Carbon Finance

🔑 Solution: Add diversification with international funds, small-cap funds, or REITs to balance your exposure.

Section 4. What I’d Do If I Were Starting Today: Step by Step

If I were starting fresh today, I wouldn’t waste time chasing trends or trying to outsmart the market. I’d take a disciplined, methodical approach tailored to different stages of life.

This phased plan focuses on building wealth in the accumulation years, preserving it as you approach retirement, and generating sustainable income once you’ve retired. Here’s how it breaks down:

Phase 1: Accumulation (Building the Foundation)

This is the wealth-building stage, where your focus should be on maximizing savings and letting compounding work its magic. For most people, this phase spans their 20s, 30s, and 40s.

1. Max Out Tax-Advantaged Accounts

Start with accounts like:

401(k): Contribute at least enough to capture your employer’s match (it’s free money). Then aim to max it out ($22,500 annually in 2024, or $30,000 if you’re 50+).

Roth IRA: If you’re under the income limit, prioritize maxing this out for tax-free growth. In 2024, the limit is $6,500 annually ($7,500 if 50+).

HSA: If you’re eligible, treat your HSA as a stealth retirement account. Contributions are pre-tax, investments grow tax-free, and withdrawals for medical expenses are also tax-free.

Tax-advantaged accounts are the cornerstone of FIRE because they defer or eliminate taxes, allowing your investments to grow faster.

2. Focus on Broad Market Exposure

Invest in diversified, low-cost index funds that provide exposure to both U.S. and international markets:

Vanguard Total Stock Market ETF (VTI): Covers the entire U.S. stock market, providing exposure to large-, mid-, and small-cap stocks.

Schwab International Equity ETF (SCHF): Adds global diversification, reducing your reliance on the U.S. market.

These funds minimize risk while capturing the long-term growth of the global economy.

3. Automate Contributions

Automation is your secret weapon. Set up recurring contributions to your 401(k), Roth IRA, or brokerage accounts. This ensures you stay consistent, even during market downturns or when life gets busy. Automation also eliminates emotional decision-making, which is where most investors go wrong.

Phase 2: Pre-Retirement (Preservation and Transition)

This phase begins roughly 5-10 years before your target retirement date. The focus shifts from aggressive accumulation to preserving your nest egg and preparing for the income stage.

1. Adjust Your Asset Allocation

As you approach retirement, you’ll want to reduce your exposure to market volatility. Shift 10-20% of your portfolio into bonds or cash reserves to provide stability. Consider:

BND (Vanguard Total Bond Market ETF): For broad bond market exposure.

Treasury Inflation-Protected Securities (TIPS): To hedge against inflation.

High-Yield Savings Accounts or Money Market Funds: For immediate liquidity.

This doesn’t mean abandoning equities altogether. Stocks are still crucial for growth and keeping ahead of inflation, but bonds provide a buffer during market downturns.

2. Optimize Taxes

Pre-retirement is the perfect time to implement tax strategies that can significantly impact your financial independence:

Roth Conversions: If you expect to be in a lower tax bracket during early retirement, convert a portion of your traditional IRA or 401(k) into a Roth IRA. This creates a tax-free income stream in retirement.

Tax-Loss Harvesting: If you hold investments in taxable accounts, sell underperforming positions to offset capital gains. Reinvest in similar assets to maintain exposure while capturing the tax benefit.

3. Practice Living on Your Withdrawal Rate

Before you officially retire, test your budget. Start living on the amount you plan to withdraw annually from your portfolio (e.g., 4% of your projected nest egg). This exercise helps identify any gaps in your spending plan and gives you time to adjust before relying on your investments entirely.

Phase 3: Retirement (Sustainability and Income)

Once you’ve reached financial independence, the focus shifts to creating a sustainable income stream while preserving your capital. This phase is all about balance—enjoying the wealth you’ve built without depleting it prematurely.

1. Use a Bucket Strategy for Stability

The bucket strategy helps mitigate sequence-of-returns risk, which occurs when you withdraw funds during a market downturn. Here’s how to structure it:

Bucket 1: 3-5 years of living expenses in cash or short-term bonds. This provides a safety net during market volatility.

Bucket 2: The remainder of your portfolio in equities for long-term growth. Funds like VTI (U.S. total market) and VXUS (international stocks) are ideal for this purpose.

This approach ensures you’re not forced to sell stocks at a loss during a bear market.

2. Stick to the 4% Rule—But Stay Flexible

The 4% rule is a guideline for sustainable withdrawals. For example, if you retire with $1 million, withdrawing $40,000 annually gives you a high probability of not outliving your money. However, flexibility is key. In years when markets are down, consider reducing withdrawals to preserve your portfolio.

3. Tax-Efficient Withdrawals

Retirement is all about minimizing taxes on your income. Follow this sequence to optimize withdrawals:

Taxable Accounts: Tap these first, since they’ve already been taxed.

Tax-Deferred Accounts: Withdraw from traditional IRAs or 401(k)s once required minimum distributions (RMDs) begin.

Roth Accounts: Save these for last to let them grow tax-free as long as possible.

This phased plan is the culmination of everything I’ve learned from years of managing portfolios, optimizing taxes, and navigating unpredictable markets. It’s not just a strategy—it’s a framework designed to grow with you, adapting as your financial situation evolves.

The true genius of index funds lies in their efficiency. They strip away the noise, eliminate unnecessary costs, and let you focus on the essentials: saving consistently, staying invested, and letting time and compounding do the hard work.

This isn’t about chasing the next big win or trying to outsmart the market—it’s about taking control of your financial future. It’s about mastering a system that’s proven to work, regardless of market conditions or trends.

Start now. Stay disciplined. Trust the process.

Over time, you’ll see how the power of compounding doesn’t just transform your portfolio—it transforms your life.

Wealth isn’t built in a day, but with the right strategy, it’s inevitable.

Thank you for reading!

- Mike

Exactly, timing doesn't work - as someone who tracks institutional money flows daily, I can confirm your point about market reversals, since I consistently see the biggest institutional buying volumes exactly when retail investors are panic-selling during downturns.