Using IRS Rules Against Themselves to Add $204,000 to Your Retirement

Last December, 4 million Americans were forced to liquidate $47 billion worth of dividend stocks.

That’s because at 73, the IRS forces you to withdraw money from your IRA.

Most see this as a tax penalty that kills their income strategy.

Instead, I'll show you how to make RMD requirements add $204,000 to your retirement income.

Last month, I sat down with a client - let's call him Tom - who just got his first RMD notice.

His traditional IRA: $1.2 million.

Sounds great, right?

His required withdrawal: $45,283.

His tax bill on that withdrawal: $12,678.

His net cash after taxes: $32,605.

Tom stared at the numbers. "I saved all this money, but now I'm forced to take it out and pay taxes I don't want to pay on money I don't need to spend."

Welcome to the RMD trap.

It's hitting 4 million Americans this year alone.

But here's what Tom didn't realize - and what most financial advisors never mention: those forced withdrawals create a huge income arbitrage opportunity.

What RMDs Really Mean Beyond the Tax Talk

At age 73, the IRS forces you to withdraw roughly 3.8% of your traditional IRA balance.

Every year after that, the percentage goes up.

By 80, you're pulling out 5.3%.

By 85, it's 6.8%.

The Real Problem is that most people have their money in the wrong accounts doing the wrong things.

They've got $500,000 in a traditional IRA earning 2% in conservative funds. When RMDs hit, they're forced to withdraw money from their lowest-yielding assets while paying taxes at their highest rates.

Smart money does this backwards — this is what I teach my clients.

They systematically move money from accounts with forced withdrawals (traditional IRAs) into accounts with no withdrawals required (Roth IRAs) while upgrading the underlying investments.

Instead of being forced to sell 2% bond funds, they're harvesting 7% dividend yields tax-free.

The December Liquidation Pattern

Here's something I notice yearly for two decades: every December, quality dividend stocks get systematically hammered.

But not because of fundamentals. Because of forced selling.

December is RMD season.

Forced IRA withdrawals must be satisfied by December 31st. Millions of retirees sell first and ask questions later, creating predictable "flash sales" in dividend darlings.

They don't care about timing. They need cash.

Three Recent Examples:

The Pattern:

This happens every year in different stocks. Utilities, consumer staples and REITs consistently get hit because they're popular in retirement accounts.

The Opportunity:

If you understand the forced selling calendar, you can position yourself as the buyer when others are forced sellers.

Most people think about RMDs wrong — they focus on the withdrawal.

The real game is about asset location - what you own where.

Traditional Thinking:

Put conservative investments in IRAs because "you don't want to take risks with retirement money."

Income Reality:

That's exactly backwards. If you're going to be forced to withdraw money, why not be forced to withdraw from your highest-yielding positions?

Better Approach:

Traditional IRA (forced withdrawals): High-dividend positions you're comfortable selling pieces of annually. Realty Income at 5.8%. AT&T at 6.4%. Utility funds yielding 4-5%.

Roth IRA (never forced out):

Growth dividends and volatile high-yielders you want to compound forever. Apple's dividend growing 8% annually. Microsoft's dividend growing 11% annually. BDCs yielding 10%+ that swing wildly but compound beautifully over time.

Taxable accounts:

Tax-efficient index funds and covered call opportunities where you control the timing.

The Math:

Same $500,000 portfolio.

Traditional approach might generate $15,000 annually with half going to taxes. Optimized approach generates $22,000 annually with better tax treatment.

This Is Critical — The Roth Conversion Window

Here's the move that separates amateurs from pros: strategic Roth conversions in your 60s.

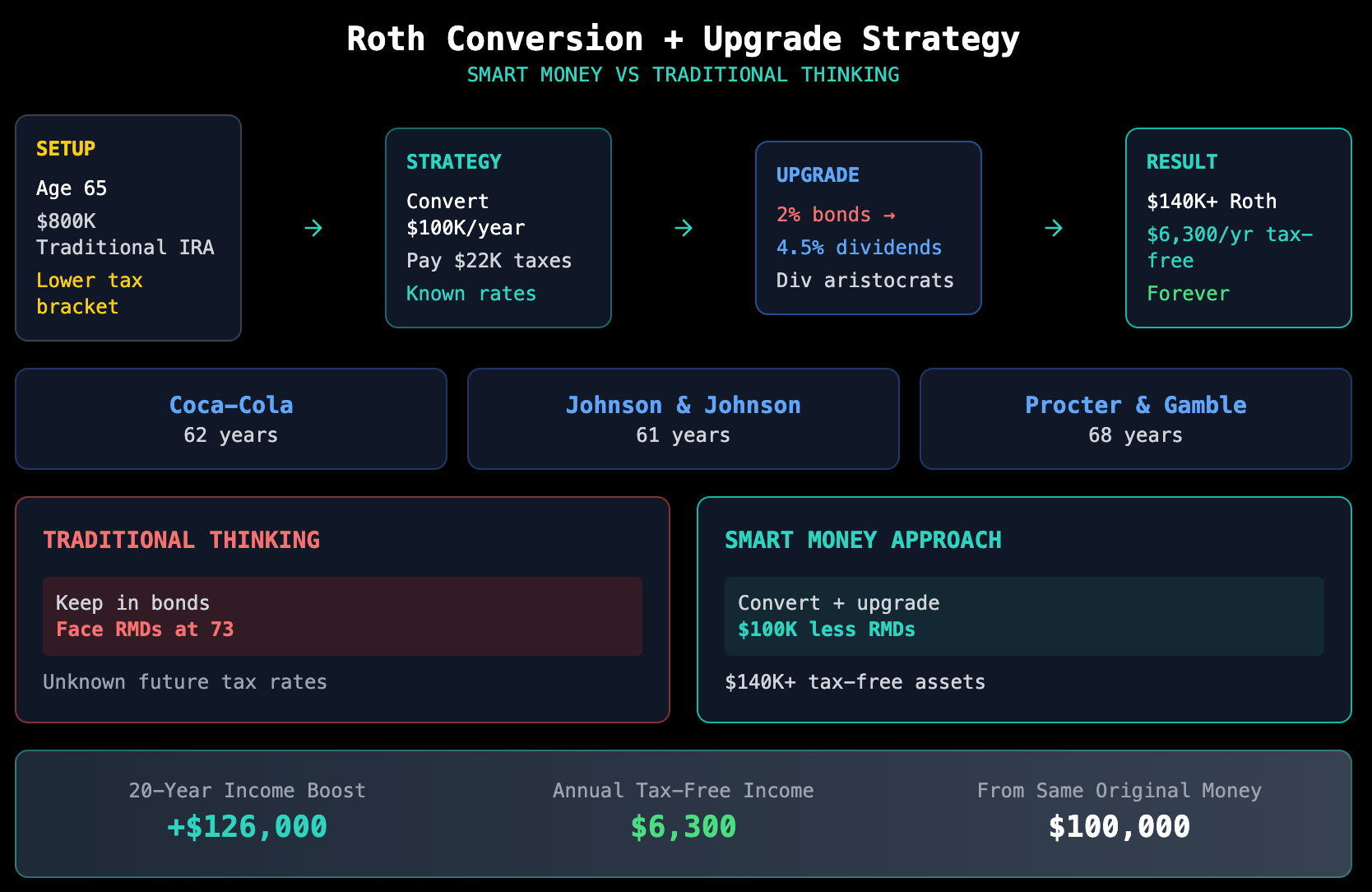

The Setup:

You're 65. You've got $800,000 in traditional IRAs.

Your income dropped after retirement, so you're in a lower tax bracket than you'll be in later (when Social Security kicks in and RMDs start).

The Strategy:

Systematically convert $80,000-$100,000 annually from traditional to Roth IRAs. Pay taxes now at known rates instead of unknown rates later.

The Upgrade:

Don't just convert. Improve what you own in the process.

Move that money from conservative bond funds into dividend-growing assets. Coca-Cola raising dividends for 62 straight years. Johnson & Johnson for 61 years. Procter & Gamble for 68 years.

Real Numbers:

Convert $100,000 from a 2% bond fund to a portfolio averaging 4.5% dividend yield. Pay $22,000 in taxes (22% bracket).

Result: In 8 years when RMDs would start, you've got $100,000 less in forced withdrawals but $140,000+ in Roth assets generating $6,300 annually tax-free.

Forever.

Over 20 years of retirement, that's $126,000 more income from the same original money.

And once you hit 70.5, there's a little-known rule that creates serious income opportunities: Qualified Charitable Distributions (QCDs).

You can send up to $108,000 annually directly from your IRA to charity. It counts toward your RMD but doesn't count as taxable income.

Why This Matters:

It lets you redirect money that would have gone to taxes.

The Play:

You're 75 with a $30,000 RMD requirement. You normally give $8,000 annually to charity.

Traditional approach: Take $30,000 RMD, pay $7,200 in taxes, give $8,000 to charity from after-tax money.

QCD approach: Send $8,000 directly from IRA to charity, take $22,000 for yourself, pay $5,280 in taxes.

Result:

Same charitable giving, $1,920 less in taxes. Use that savings to buy more dividend stocks in your taxable account.

Over 15 years, that's $28,800 more working in income-producing assets instead of going to Uncle Sam.

The Covered Call Enhancement Strategy

Here's where RMDs get interesting for income investors.

If you're going to be forced to sell shares anyway, why not collect option premiums while you wait?

The Setup:

You own 1,000 shares of Realty Income in your traditional IRA. Current price: $58. Your RMD requires selling 200 shares this year.

The Enhancement:

Sell covered calls against those 200 shares at $60 strike price expiring in 3 months. Collect $800 in premium income.

Scenario 1: Stock stays below $60. Keep the premium, keep the shares, sell them later for RMD.

Scenario 2: Stock goes above $60. Shares get called away at $60 (exactly what you needed for RMD anyway), plus you keep the $800 premium.

Result:

Either way, you're generating extra income from shares you were going to sell anyway.

Advanced Move: Use the option premium to buy more shares in your Roth IRA. You're essentially converting forced-sale proceeds into tax-free growth assets.

Making This Systematic:

The beauty of systematic covered calls in RMD planning: you're collecting extra income on positions you might liquidate anyway. Whether the stock gets called away or you sell for RMD requirements, you keep every premium dollar.

But you need the sweet spot: quality dividend stocks with liquid options and volatility premiums worth harvesting.

Premium subscribers get my Thursday put picks and Sunday call setups - from my VADER screening algo, which analyzes 3,200+ stocks, hunting for volatility arbitrage opportunities that boost income.

Recent covered call results show why this approach works:

The Early Withdrawal Strategy (Before 73)

Most people think you can't touch IRA money before 59.5 without penalties.

Wrong.

There's a lesser-known rule called "substantially equal periodic payments" (SEPP or Rule 72t) that lets you take early withdrawals penalty-free if you follow specific formulas.

Why Consider This:

If you retire early but have most of your money in traditional IRAs, you might want to start systematic withdrawals in your 60s rather than waiting for forced RMDs.

The Advantage:

You control the timing and amount instead of the IRS controlling it later.

The Strategy:

Calculate periodic payments that keep you in lower tax brackets while systematically moving money to Roth or taxable accounts with better assets.

Warning: This locks you into payments for 5 years minimum. But for the right situation, it beats getting hammered by large RMDs later.

3 Massive Mistakes to Avoid

Mistake #1: Waiting Until 73 to Plan

I see this constantly.

People ignore RMDs until the year they kick in, then panic. By then, most of your options are gone.

Start planning at 60.

Execute strategies in your 60s.

Optimize what's left in your 70s+.

Mistake #2: Converting Everything at Once

Some folks get excited about Roth conversions and try to move everything in one year. Bad move.

You'll spike into higher tax brackets and trigger Medicare surcharges.

Slow and steady wins.

Spread conversions over multiple years to optimize tax rates.

Mistake #3: Keeping the Same Investments

The biggest missed opportunity: converting from low-yield to low-yield assets.

If you're moving money from traditional to Roth IRAs, upgrade what you own in the process.

2% bond funds to 5% dividend aristocrats.

Conservative balanced funds to strategic REIT positions.

Make the tax cost worth it.

Current tax rates expire after 2025.

The 22% bracket becomes 25%. The 24% bracket jumps to 28%.

Every Roth conversion you delay gets more expensive.

Every year you wait to optimize RMD strategies costs more money.

Plus, with $34 trillion in national debt, in which direction do you think tax rates are headed long-term?

Ok, so what’s the next move? — Depends on Your Age

Ages 55-65:

Model your future RMD requirements. Start small Roth conversions to test the process. Build your dividend stock watchlist for conversion opportunities.

Ages 65-72:

Execute systematic conversions. This is your golden window before RMDs start. Focus on moving money into higher-yielding assets during the conversion process.

Ages 73+:

Optimize remaining traditional IRA positions for income generation. Use QCDs if you're charitably inclined. Focus on tax-free growth in Roth accounts.

For Everyone: Understand the seasonal patterns. December selling creates January buying opportunities. Position yourself accordingly.

Let me show you how this actually works:

Baseline Scenario:

$1 million traditional IRA, taking standard RMDs, paying taxes at 24% bracket.

Age 73 RMD: $37,700

Taxes: $9,048

Net income: $28,652

20-year total after taxes: $687,500

Optimized Scenario:

Same starting point, but strategic conversions in 60s and asset optimization.

Age 73: $600,000 traditional IRA, $400,000+ Roth IRA

Traditional RMD: $22,600

Taxes: $5,424

Roth withdrawals: $20,000 (tax-free)

Total net income: $37,176

20-year total after taxes: $892,200

Difference: $204,700 more income over retirement. Same original assets, better strategy.

RMDs aren't a punishment for saving successfully.

They're the biggest systematic income opportunity most investors never see.

The choice is simple: be the forced seller or be the strategic buyer.

Thank you for tuning in today and supporting my work!

Mike Thornton, Ph.D.

This is education, not personalized advice. Every situation is different. Work with a qualified advisor to implement these strategies properly. But don't wait too long to start the conversation.