How to Double SCHD’s Dividend: The 1 Trade Every Income Investor Should Know

Everyone talks about SCHD like it's the holy grail of dividend investing.

And honestly? They're not wrong.

This ETF tracks the crème de la crème of American dividend payers—writing checks to shareholders for over a decade, having rock-solid balance sheets, and operating businesses that Buffett would approve of.

SCHD currently yields around 3.81%, after taxes, that's about 3.24% hitting your checking account.

With inflation running hot, you're essentially treading water financially while hoping your shares appreciate enough to maintain your lifestyle.

Don't get me wrong—SCHD is magnificent at what it does.

With approximately 103 holdings and an estimated average payout ratio of just 61%—sustainable dividends from actual earnings, they charge only 0.06% annually, practically free by Wall Street standards. Since launching in 2011, it's delivered a staggering 430% in total returns.

But here's what bugs me: SCHD could be doing so much more for you.

Twenty years doing this have taught me that many institutions have one massive advantage over individual investors.

And it’s not necessarily better research, superior technology, or inside information. It's simpler.

They systematically rent out their upside potential for immediate cash.

Think about it like owning rental property. You could sell your house and take whatever the market gives you that day. Or you could collect monthly rent from tenants who pay you for the possibility of buying it later at a predetermined price. Same asset, completely different income stream.

That's exactly what covered calls do with your stock holdings.

Yet most individual investors have no idea they can play this same game.

Let me walk you through how to transform SCHD into an Income Machine.

So, let's say you own 100 shares of SCHD

As of mid-June 2025, that's around a $2,700 investment (at ~$27.00 per share, following a 3-for-1 split in late 2024).

Those shares currently pay you around $99.60 annually in dividends—nice, but not exactly life-changing money.

Here's where it gets interesting: Every 100 shares you own gives you the right to sell what's called a "call option." Think of this call option as a contract. You're agreeing to sell your SCHD shares to someone else at a specific price (called the "strike price") by a certain date (the "expiration").

In exchange for giving them this option, they pay you money upfront—immediately, deposited right into your account.

Now, two things can happen when that expiration date arrives:

Scenario One: SCHD's price stays below your strike price. The person who bought your call option doesn't exercise it (why would they pay your strike price when they can buy shares cheaper in the open market?). You keep your shares, you keep the money they paid you, and you can sell another call option for next month. It's like collecting rent on shares you still own.

Scenario Two: SCHD's price rises above your strike price. They exercise the option and buy your shares at the strike price. You sell your shares for a profit (remember, you picked a strike price higher than what you paid), plus you keep all the money they paid you for the option. Yes, you miss out on any gains above the strike price, but you still made money.

Either way, you win.

Now, let me show you what this looks like with actual current market data

With shares trading around $27, you can sell a call option with a $28 strike price that expires in about a month.

For selling this contract, you could collect a premium.

It's important to note that these premiums fluctuate with market volatility, but a typical premium recently might be around $0.10 per share, or $10 total for the contract.

That might not sound like much until you annualize it.

Let's look at the potential annual income:

Dividend Income: $99.60

Options Income: $10 (premium) x 12 months = $120

Total Potential Income: $99.60 + $120 = $219.60

This strategy could generate a potential annual yield of approximately 8.1% on your $2,700 investment.

But here's where the math gets really compelling after taxes:

Dividend Income (qualified): 3.81 net.

Option Income (ordinary): Our $120 in options income is a ~4.4% gross yield on our $2,700 cost. So: 4.4 net.

Total After‑Tax Yield: 3.24

Your total after-tax yield jumps from ~3.2% to over 6.5% in this setup, potentially higher when volatility spikes.

And these aren't hypothetical projections.

During periods of higher market volatility, option premiums swell considerably — it’s common to generate 8% to 10% annually just from the option premiums, before even counting the dividends.

The Three Approaches to Maximizing Your Income

Once you understand the basic concept, you can tailor the strategy to match your comfort level and income needs.

The Conservative Approach:

Involves selling call options with strike prices about 5% to 7% above SCHD's current price. You'll collect smaller premiums, but there's less chance your shares will get called away. This might generate an extra 2% to 4% annually in option income, bringing your total yield to around 6% to 8%.The Balanced Approach:

Uses strike prices closer to the current stock price—maybe 2% to 4% above where SCHD is trading. You'll collect more premium, perhaps 4% to 6% annually, but there's a higher probability your shares will get sold if SCHD rallies. Total yield potential: 8% to 10%.The Aggressive Income Approach: Involves selling options right at or even slightly below the current stock price. This maximizes your premium income—potentially 6% to 9% annually—but makes it much more likely your shares will get called away. Total yield potential: 10% to 13%.

The beauty is that you control the dial.

Want more income → Move your strikes closer to the current price.

Want to keep your shares → Move the strikes further away and accept lower premiums.

But every strategy has trade-offs...

...and covered calls have two main ones that you need to understand going in.

The first risk is opportunity cost.

When you sell a call option, you're capping your upside at the strike price.

So, if SCHD unexpectedly rockets higher, you'll miss those gains above your strike.

But here's the thing—SCHD isn't exactly known for meme-stock volatility. This is a fund of steady, mature dividend payers. The companies in SCHD are more likely to grind higher steadily than to gap up 20% overnight. That makes them ideal candidates for this strategy.

The second risk is assignment.

This is having your shares called away when you'd prefer to keep them, which happens when SCHD's price rises above your strike price at expiration. But here's a perspective shift: getting assigned isn't actually a bad thing. You sold your shares for a profit (remember, you chose a strike price above your cost basis), plus you kept the option premium. You made money. If you want to continue the strategy, you simply buy the shares back and start over.

The mechanics of actually doing this

It’s simpler than most people assume.

You'd need a brokerage account that allows "Level 2" options trading, which covers covered calls.

Once approved, here is a clear, step-by-step example of the trade we discussed:

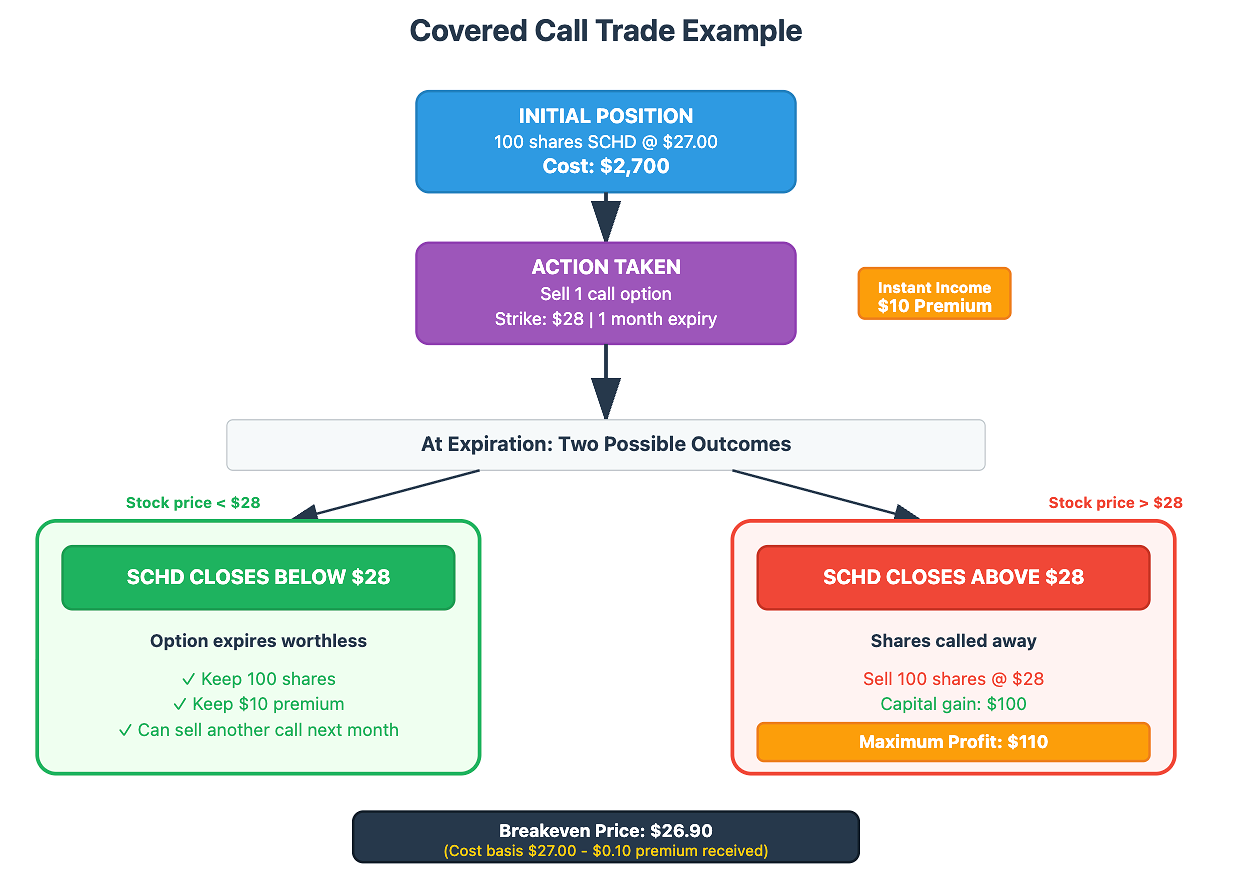

Your Position: You own 100 shares of SCHD.

Your Cost Basis: $27.00 per share ($2,700 total).

Your Action: You sell one call option contract with a $28 strike price and a one-month expiration.

Your Income: You receive a $10 premium ($0.10 per share) instantly.

Now, let's analyze the potential outcomes:

If SCHD closes below $28: The option expires worthless. You keep your 100 shares and the $10 premium.

If SCHD closes above $28: The option is exercised. You sell your 100 shares for $28 each. Your Maximum Profit is the capital gain plus the premium: ($28 sale price - $27 cost basis) x 100 + $10 = $110.

Your Breakeven Price on the position is your cost basis minus the premium: $27.00 - $0.10 = $26.90. As long as SCHD stays above this price, the trade is profitable.

Most successful practitioners develop a routine.

They might sell 30- to 45-day options each month.

When an option expires worthless, they immediately sell a new one.

When shares get assigned, they evaluate whether to buy them back or deploy the capital elsewhere.

And once you're comfortable with the basics, there are several ways to optimize the strategy further

→ Rolling techniques let you avoid assignment. If your call option becomes profitable for the buyer, you can "buy it back" and simultaneously sell a new option with a later expiration date.

→ The hybrid approach involves using only part of your SCHD position for covered calls. Maybe you sell calls against 100 shares while holding another 100 shares "naked" to capture unlimited upside.

→ Some investors combine covered calls with cash-secured puts—selling put options on SCHD while they wait to buy shares at lower prices. This creates income from both directions.

But, before you implement this yourself...

...you should know about the ready-made alternatives.

Several ETFs now offer exposure to covered call strategies, such as DIVO, JEPI, and QYLD.

These can be convenient solutions, but they come with trade-offs.

You pay higher fees, lose control over the timing and strikes, and often get stuck with whatever underlying holdings the fund managers choose.

The DIY approach gives you complete control while keeping costs minimal.

You can take a solid dividend ETF and make it work harder for you.

Yet, most accept whatever yield the market gives them.

But with a little knowledge and effort, you can potentially double that income using the exact same conservative holdings.

Thank you for tuning in today and supporting my work!

Mike Thornton, Ph.D.

Thanks Mike. Another enjoyable read.

You're on fire this week Mike with these high value posts!

I was just wondering since we are on the topic of the risks with selling CC how would your strategy change/adapt in the following situation. Let's say you have bought 100 shares in company X after checking valuations and the company has passed all your filters, and the option income provides a good risk/reward. You buy the shares and sell the CC but during the life of the option the price tanks. Maybe it's due to some surprise event, and it drops fast enough that you are not able to effectively roll out the call. The CC expires worthless but you are down a significant amount, let's say the stock has dropped 15%, while you are better off for having sold the call, you are still underwater.

So here is the question, what would you do in terms of the CC strategy at this point? You could sell another CC but the strike price will be below your entry price, hence if the shares are called away you will be selling at a loss. I understand the circumstances will dictate what to do, you would need to reevaluate the company and see if it's worth hanging onto the shares or not. But if you do decide to keep them, would continue to sell calls on it?