Buffett’s Cash Strategy: Safe, Liquid, ~3.9% Yield

T-Bill Ladders for Yield, Liquidity, and Control

A lot of people I talk to keep more cash than they’d like.

Not because they love cash, but because they want flexibility.

They want money available for opportunities, emergencies, or just peace of mind.

The downside is obvious. Most of that cash earns next to nothing.

When institutions handle cash, they spread it across short maturities so something is always coming due, and the money stays liquid without being idle.

Therefore, in this piece, I’ll show you:

how to make this work for the individual retail investor with T-Bill Ladders

explain what it pays today

and how to set it up so it stays flexible and easy to manage.

What a T-Bill Ladder Is, and Why People Use It

A T-bill is a simple way to hold cash without letting it go stale.

Instead of putting everything into one bill or leaving it idle, you spread the money across several short-term Treasuries.

Each one matures at a different time.

The benefit is very practical: when one bill matures, the cash shows up in your account and you decide what to do with it.

Reinvest it. Use it. Move it.

You’re never locked in for long, and you’re always earning something while you wait.

People use T-Bill ladders for three main reasons:

Yield. Short-term T-bills usually pay more than typical savings accounts.

Access. Because the maturities are staggered, some of your cash frees up regularly.

Control. You can roll each maturity into a new bill at whatever rate the market is offering at that moment.

Professionals do this all the time.

They don’t keep large piles of cash sitting around. They break it up, put it into short maturities, and keep a steady flow of liquidity coming in.

Warren Buffett, for example, directs Berkshire Hathaway to hold a massive portion of its cash—often hundreds of billions of dollars—in U.S. Treasury bills.

He views them as the ultimate safe, liquid “ammunition” to be deployed quickly when big investment opportunities arise. For individual investors, the T-bill ladder simply translates this professional strategy to a smaller, more manageable scale.

For anyone running an income-focused portfolio, it’s the same idea.

Cash stays safe. It stays available. And it actually earns.

It’s a simple upgrade that fits into the real world, without you having to babysit it.

What T-Bill Ladders Pay Right Now

As of November 2025, short-term Treasury yields are still solid.

Not the peak levels we saw a year ago, but high enough to make a real difference.

Here’s the rough range:

4-week T-bill: around 3.9 percent

13-week T-bill: around 3.8 percent

26-week T-bill: around 3.7 percent

A ladder built across these maturities usually ends up in the high-3 percent range.

That’s the “real world” yield you can expect without doing anything complicated.

How does that compare to the usual cash options?

High-yield savings: roughly 3.5 to 4.3 percent.

Short-term CDs: around 4.1 to 4.3 percent for 3 to 6 months.

Money market funds: roughly 3.7 to 3.9 percent after fees.

So a simple ladder is competitive with the very best savings products on the market.

And unlike CDs, you’re not locking anything up.

The money comes back to you on a schedule you set.

You’ll see this theme a lot in the rest of the article.

A T-bill ladder doesn’t try to beat the market or squeeze out an extra tenth of a percent. It just makes sure your cash earns a fair rate while staying available for emergencies, expenses, or CSP Collateral.

From my experience, for most people, that’s already a big improvement over how cash usually sits in their account.

How Weekly Rollovers Actually Work

A T-bill ladder sounds abstract until you see what it does week by week.

The idea is simple: you break your cash into pieces, put each piece into a short-term bill, and let the maturities create a steady rhythm.

When one bill matures, the cash lands in your account.

You either roll it into a new bill or use it if you need it.

Rates move up and down, but because you’re reinvesting regularly, you’re always picking up the current short-term yield.

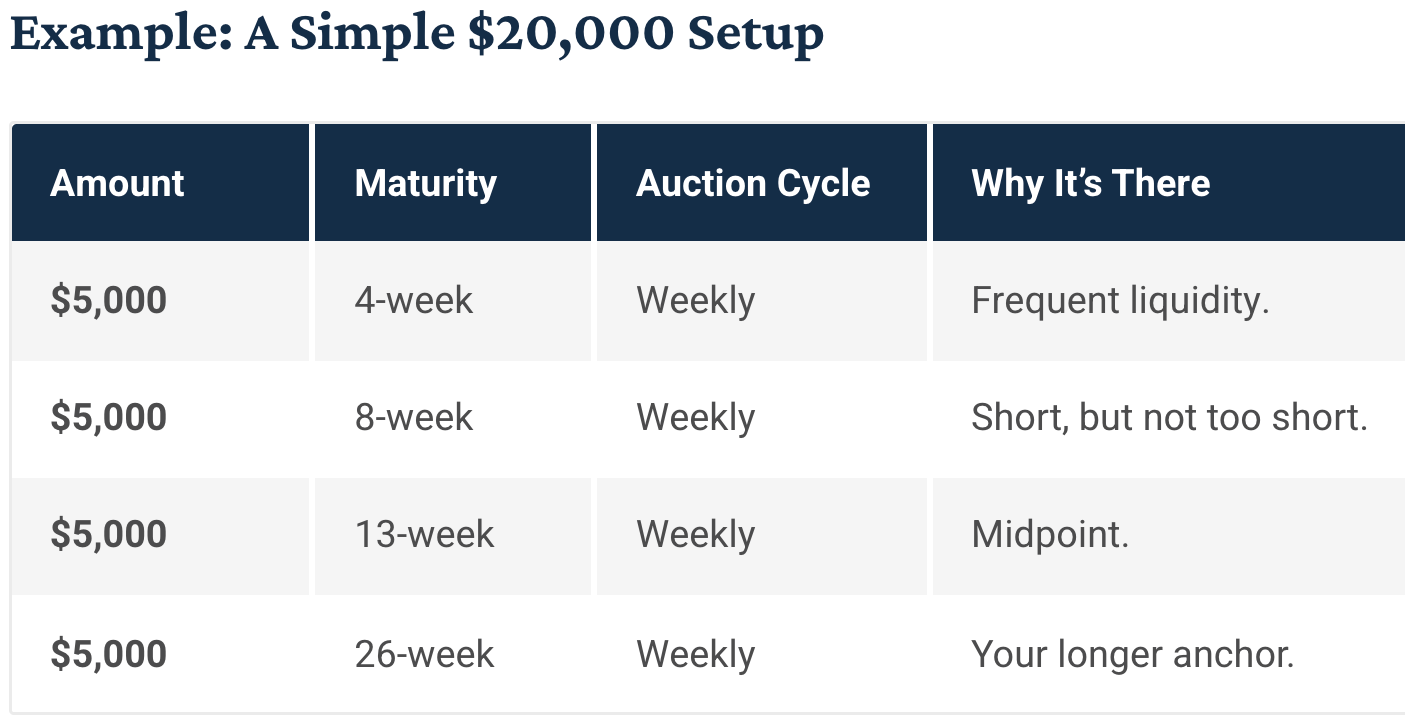

Here’s a small example using $20,000 split across five maturities:

Example Ladder Setup

After the initial setup, these maturities start creating a predictable cycle.

Cash shows up every few weeks. If you want a tighter rhythm, you can build a weekly ladder instead. Same idea, just smaller increments.

The benefits become obvious:

Your cash always earns.

You always have liquidity on the calendar.

You aren’t stuck with yesterday’s interest rate.

You can stop rolling anytime you need the money.

There’s nothing to babysit. You just handle each maturity when it comes up.

Safe, liquid, and always earning.

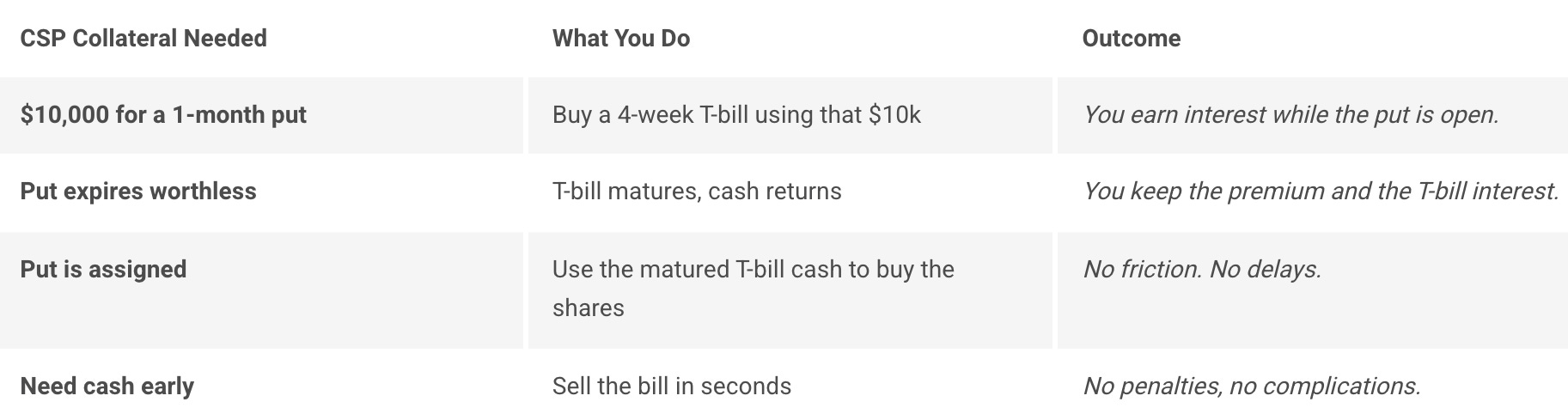

How T-Bills Boost Cash-Secured Put Income

If you sell cash-secured puts, you already know the drill.

You set aside cash in case you’re assigned.

Most people let that cash sit there doing nothing.

It’s the least productive part of the whole strategy.

A T-bill ladder fixes that without changing how you trade.

Short-term Treasuries count as acceptable collateral at most major brokers. That means the money you use to secure a put can sit in T-bills instead of a low-yield sweep account. When the option expires or gets close to assignment, the bills either mature into cash or can be sold immediately with no drama.

Here’s why this matters.

You earn while you wait. If you’re posting $10,000 as collateral, it’s better earning 3.8–4 percent in T-bills than 0.1 percent in a sweep.

The timing works cleanly. You can line up T-bill maturities with option expiration dates so the cash is available when you need it.

There’s no extra risk. These are Treasuries. If you need the cash, you sell the bill or let it mature. The broker treats it like cash for this purpose.

To make this concrete, here’s a simple version of what many income traders do:

If you repeat this every month, that extra interest stacks up. It doesn’t change the risk of the put. It just makes the dead collateral a little less dead.

This is the same idea institutions use. They never let reserves sit idle.

They keep them in short paper and pull money when they need it.

Regular investors can do the same thing on a smaller scale with no new skills required.

The main point I am trying to make is very simple:

If your collateral is sitting around anyway, it should earn.

A T-bill ladder does that quietly in the background while you keep running your normal put-selling process.

How to Set Up a Ladder

Here’s the basic idea.

T-bills come in short maturities: 4, 8, 13, 17, and 26 weeks.

These are auctioned on a weekly cycle. You place a non-competitive bid through your broker or TreasuryDirect, and the system fills your order at the final yield.

It’s very straightforward and takes a few clicks.

A simple way to get started is to break your cash into a few pieces and buy different maturities:

Some very short (4 or 8 weeks)

Some in the middle (13 or 17 weeks)

One on the longer end (26 weeks)

You’ll end up with a small calendar of maturities.

When the first one comes due, the cash lands in your account.

At that point, you choose whether to roll it into a new bill or keep it available.

If you want a weekly rhythm, you can build it by spacing your first few purchases a week apart. You don’t need special tools for this. Your broker already shows the upcoming auction dates, and most platforms also offer an auto-roll option.

If you turn that on, the system reinvests each maturity automatically.

Here’s what this looks like in practice:

From here, the ladder runs itself.

A bill matures, you reinvest or keep the cash.

No penalties. No lockups. No timing stress.

And unlike CDs, you’re not stuck if your needs change.

The goal is consistency.

You want your cash earning, and you want predictable liquidity, and you want a system you don’t have to babysit.

A T-bill ladder checks all three boxes with almost no maintenance.

When people try this once, they usually stick with it.

It’s simple, it pays, and it removes that uncomfortable feeling of cash sitting around doing nothing.

Because if your money is going to sit somewhere, it might as well earn.

If you found this article helpful, please tap the ❤️ below or share it with a friend.

Thank you for reading and for being a part of The Multiplier.

— Mike

I use Schwab’s money market or SGOV. That way I can have the money the next day anytime I need it. With SGOV I can have it in a minute. with Schwab I get daily interest and SGOV pays once a month dividend so you do loose some interest.