How VADER Works

The 5-stage screening engine behind every setup in The Multiplier — how 500,000+ option contracts become 25–40 actionable picks before the market opens.

The hardest part of selling options for income isn't learning the strategy.

It's finding the right contract on the right stock on the right day.

Get that wrong, and you end up owning a stock you never wanted, at a price that no longer makes sense, in a market that's moving against you.

That's the problem VADER was built to solve.

What VADER Is

VADER — Volatility Adjusted Delta Efficiency Ranking — is the screening engine that generates the trades for The Multiplier.

It’s a proprietary, multi-step screening system built on institutional risk standards.

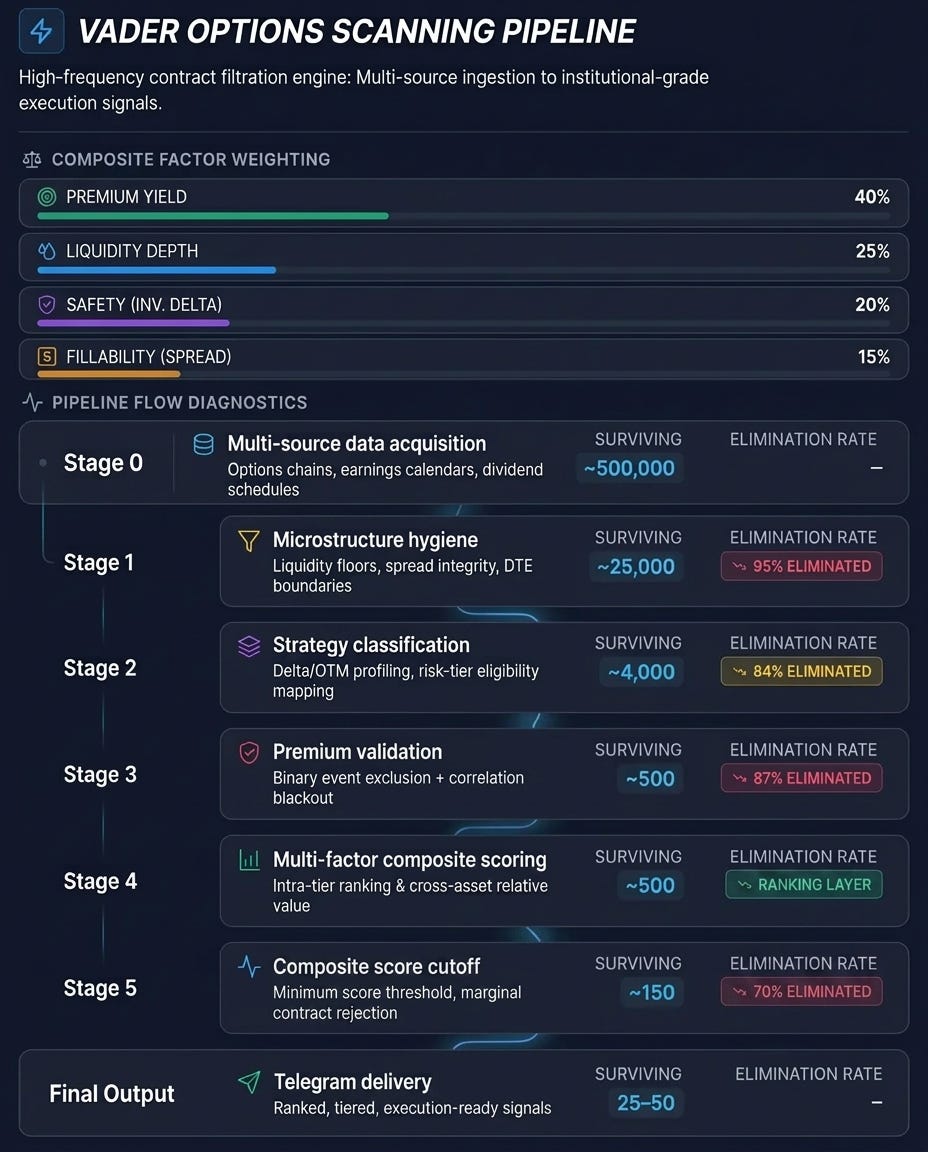

Every morning before the market opens, VADER scans 500,000+ currently listed option contracts across 595 quality stocks and ETFs.

Each contract is then stress-tested through a five-stage elimination pipeline — a sequential filter stack that enforces liquidity minimums, delta boundaries, premium thresholds, and event exclusions.

Most contracts fail immediately.

That’s intentional.

The rejection rate is brutal by design.

Roughly 0.005% of contracts survive. For every 100,000 contracts scanned, approximately five reach your screen.

Why this matters

On any given morning, there are over 500,000 option contracts available.

Most are junk. Wide spreads, no liquidity, earnings next week, premium that doesn't justify the risk.

Your brokerage platform might show you thousands of them. A free screener might narrow it to hundreds. But none of them tell you which five are actually worth your capital today.

The hardest part of options selling isn’t the strategy. It’s finding the right contract on the right stock at the right time. You could spend an hour filtering manually. VADER does it before you finish your coffee.

The Five-Stage Pipeline

Here’s why those filters matter.

They’re designed to remove the trades that look good on paper but trade badly in real life.

Stage 1 — Microstructure Hygiene

The first pass drops structurally bad or illiquid contracts.

Open interest below 100? Gone.

Bid-ask spread wider than 20%? Gone.

Expiration outside the 7–60 day window? Gone.

Strike price unreasonably far from the current stock price? Gone.

This stage alone eliminates roughly 95% of all contracts.

What it protects you from: getting trapped in wide spreads you can't exit cleanly.

Stage 2 — Strategy Classification

Surviving contracts are classified as either covered call or cash-secured put candidates, then mapped against three risk profiles: Conservative, Balanced, and Aggressive.

Each profile has specific delta ranges, OTM (out-of-the-money) requirements, and expiration windows.

A contract that’s appropriate for a Balanced profile might be too aggressive for Conservative. VADER tracks which profiles each contract qualifies for — and drops anything that doesn’t fit at least one.

Another 84% of survivors are eliminated here.

What it protects you from: taking on more delta risk than your profile can handle — or holding a contract that doesn't match your strategy.

Stage 3 — Premium Validation and Event Risk

This is the strictest stage. Three things happen:

First, premium floors.

Every contract must pay enough to justify the risk — measured both as a percentage of collateral and as a daily premium rate. If the math doesn’t work, the contract is dropped.

Second, event risk.

If the underlying stock has earnings or an ex-dividend date before the option expires, the contract is rejected. No exceptions.

This is the rule most DIY traders skip. It's also the one that causes the worst losses. A stock that drops 15% on an earnings miss doesn't recover on your timeline. For a retiree, that's not a temporary setback. It's capital you can't afford to lose.

ETFs are exempt from earnings blackouts. VADER also uses an earnings cluster system — if a major company like NVDA reports earnings, related stocks in the same sector that tend to move in sympathy are also flagged.

Third, sigma moneyness.

VADER checks whether the strike is far enough from the current stock price in volatility-adjusted terms. A contract that looks safely out-of-the-money on a calm stock might be dangerously close on a volatile one. If the buffer isn’t wide enough relative to the stock’s implied volatility, it’s removed.

This stage also enforces stricter spread limits (tightened from 20% to 15%) and applies beta caps per risk profile.

87% of remaining contracts are eliminated here.

What it protects you from: earning too little premium for the risk, getting blindsided by earnings or ex-dividend dates, and holding positions that are closer to the money than they appear.

Stage 4 — Composite Scoring

No contracts are dropped at this stage. Instead, every survivor is scored using a weighted composite:

→ Premium yield: 40%

→ Liquidity depth: 25%

→ Safety (inverse delta): 20%

→ Fillability (spread + volume): 15%

Plus adjustments for IV rank and IV-to-beta efficiency — rewarding contracts where implied volatility is high relative to the stock’s systematic risk.

The output is a ranked list, sorted by score.

What it does for you: puts the best risk-adjusted opportunities at the top of your screen so you're not guessing which setup deserves your capital.

Stage 5 — The Cut

Roughly 70% of remaining contracts are eliminated here.

Any contract below a minimum composite score is dropped.

It doesn’t matter that it passed every earlier filter - if the score isn’t high enough, it doesn’t get published.

Most screeners skip this step. They hand you a ranked list of 150 results and leave you to figure out where “good” ends. VADER makes that call for you.

The setups that survive are published to the Telegram channel before the market opens - giving you time to review, check live quotes at your broker, and decide what fits before placing an order.

What it protects you from: wading through marginal setups that passed the filters but don’t deserve your capital.

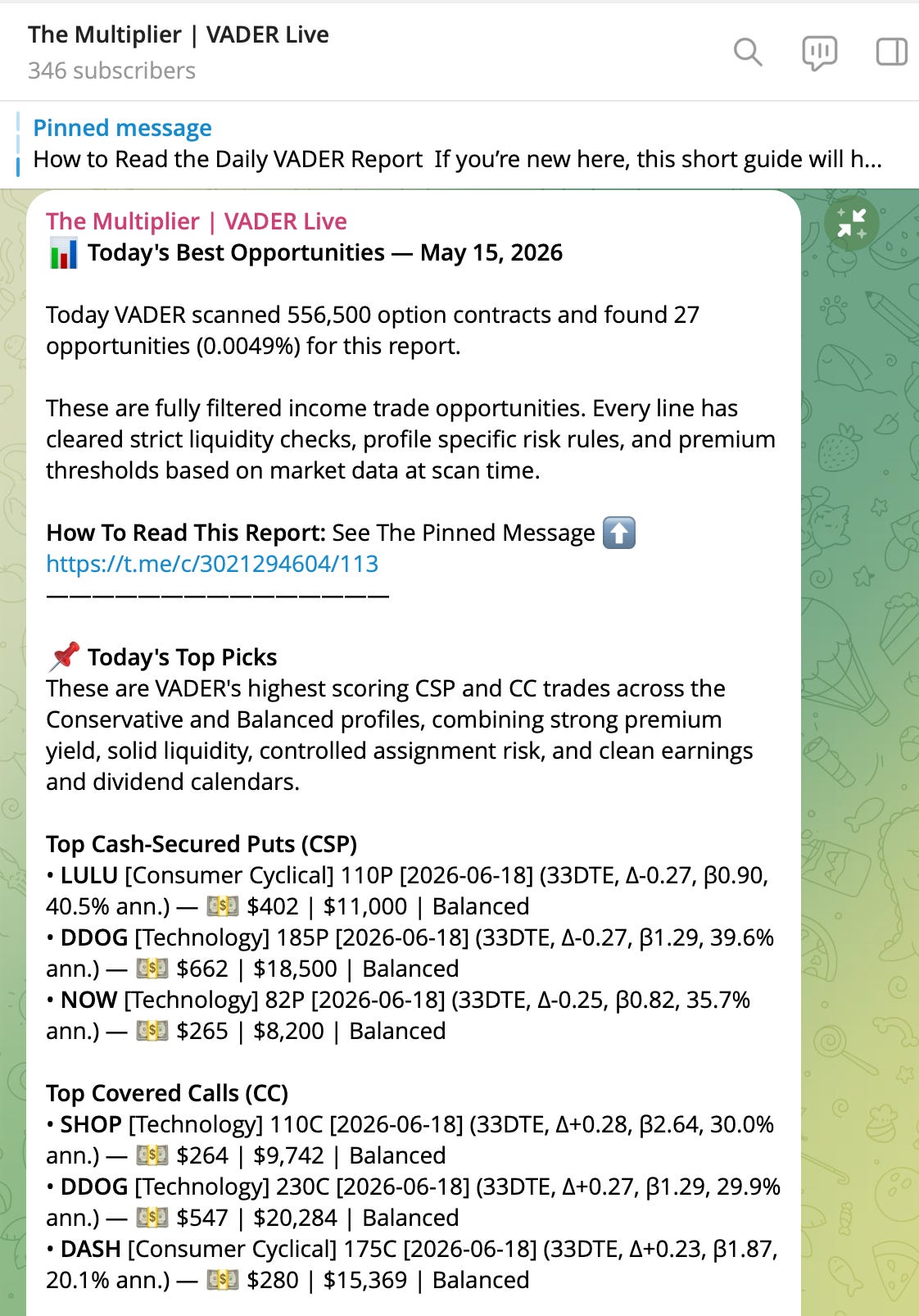

What Premium Members Get Every Morning

Each morning, I publish a short list on the Telegram channel. These are the contracts that survived the filters.

The report is organized so you can find what fits your situation quickly:

By strategy:

Cash-secured puts (CSP) and covered calls (CC) are listed separately.

By risk profile:

Conservative (lower deltas, cleaner calendars, 30–45 DTE focus), Balanced (moderate deltas, solid yield, controlled event risk), and Aggressive (shorter duration, higher deltas, faster gamma — experienced members only).

By collateral size:

Setups are grouped into brackets — under $10k, $10k–$25k, and $25k+ — so you’re not scrolling past trades that require more capital than you have available.

Every line shows the ticker, sector, strike, expiration, days to expiration, delta, beta, annualized yield, premium in dollars, and collateral required.

Your only real job at that point is selection and sizing. You’re not hunting through the entire options chain or trying to “find” trades. You’re deciding what fits your account, your available collateral, and what you already have open.

Some days, a setup fits cleanly. Other days, you pass. That choice is part of the process — not a failure to “stay active.”

Once a position is open, you manage it with a preset exit. The common approach is a standing buyback order, GTC (”Good Till Canceled”), set at your profit target.

You place it once. It sits there until it fills or you adjust it. If premium collapses to your target level, your broker closes the position automatically.

No intraday monitoring.

No refreshing quotes every hour.

Your broker does the work while you live your life.

From the Report to Your Order Screen

VADER does the filtering. You do the execution.

The setup posted at 9:45 AM is not the same setup at 1:30 PM. The stock has moved. Premium has decayed. Implied volatility has shifted. None of that means the trade is bad. It means you have a short translation job to do before you place the order.

Here’s the full sequence.

Step 1: Three checks before you open your brokerage

Before you log in anywhere, run three filters on the pick:

Can you actually take it? For a cash-secured put, that means cash on hand equal to the collateral shown in the report. For a covered call, it means already owning 100 shares of the underlying per contract. If either is missing, the trade is off the table.

Are you willing to be assigned at that strike? A CSP says: I’ll buy this stock at the strike if it drops there. A CC says: I’ll sell my shares at the strike if the stock rallies through it. If either outcome would bother you, pass.

Does the profile match yours? If the line is tagged Balanced and you run Conservative, look further down the report for a Conservative-tier alternative.

Three yeses, move on. One no, skip the trade and look at the next line.

Step 2: Pull up the options chain and validate

Log into your brokerage. Type the ticker. Go to the options chain. Filter to the expiration date shown in the VADER line.

If the report showed:

SHOP [Technology] 115C [2026-06-18] (29DTE, Δ+0.27, 31.3% ann.) - $254 | $10,239 | Balanced

You’re looking at the June 18, 2026 expiration in the chain, scrolling to the $115 strike on the call side.

Now two quick comparisons against the live data on your screen:

Is the premium within range of what VADER posted? Roughly 15% drift is normal. If VADER showed $254 and your chain shows $232 or $278, the setup is intact.

Is the strike still cleanly out of the money? For a covered call, the stock should still be below the strike. For a cash-secured put, the stock should still be above the strike.

Both checks pass, go to Step 4. One check fails, go to Step 3.

Step 3: When the conditions have shifted

Sometimes the strike no longer fits by the time you check. The stock has moved. The delta has shifted past your profile’s range. The premium has expanded or collapsed past the normal drift band.

The fix is to remember what VADER actually selected for. The specific strike number is not the point. The delta is.

VADER picks strikes inside specific delta ranges by profile:

Conservative CSP: delta -0.15 to -0.25

Balanced CSP: delta -0.25 to -0.35

Conservative CC: delta +0.15 to +0.25

Balanced CC: delta +0.25 to +0.35

If the original strike is now outside the range for your profile, slide one or two strikes up or down until you find one that lands back inside it. That’s your substitute.

A worked example. VADER posts a Balanced CSP on USO at the $70 strike, delta -0.30. By the time you check, USO has dropped a dollar. The $70 put is now showing delta -0.38, too aggressive for Balanced. You move to the $69 strike, find delta -0.27 there, and that becomes your trade. Same logic, same risk frame, different strike.

If nothing on the chain hits a clean delta with reasonable premium, skip the day. A missed setup is not a loss.

For the deeper logic of strike selection by profile, the standalone guides for cash-secured puts and covered calls cover it in full.

Step 4: Place the order

The mechanics are the same on every brokerage:

Action: Sell to Open (not Buy to Open, not Close)

Quantity: 1 contract per 100 shares of exposure

Order type: Limit (never Market)

Limit price: midpoint of the bid-ask spread

If the bid is $2.50 and the ask is $2.60, set the limit at $2.55. Submit. Not filled in ten minutes, adjust by a penny or two toward the bid.

Check the preview before final submit. The premium credit should match what you expect. The collateral hold (Fidelity calls it “estimated order value,” Schwab calls it “buying power effect”) should match the collateral figure VADER showed.

Submit. Note the position. Move on.

A one-time setup that saves you every day after

Most brokerage options chains hide delta in the default view. That makes the validation in Step 2 harder than it needs to be.

You can add delta as a visible column in five minutes, once. On Fidelity Active Trader Pro and Schwab’s thinkorswim, look for “column settings” or “customize columns” in the options chain. On the basic web platforms, it’s usually under “display preferences” or “more columns.”

Add delta. Save the view. From here on, validating a VADER pick takes thirty seconds instead of three minutes.

Real Trade Walkthrough #1: AAPL $250 Cash-Secured Put (Entry → GTC Exit → Close)

Using an actual trade from this year.

On Monday, February 2, VADER included an AAPL cash-secured put, among others. This is a classic VADER-style income trade.

Let’s walk through what that means and what happened.

First, what is a cash-secured put?

You sell a put and set aside enough cash to buy the stock if assigned. For AAPL at $250, that’s $25,000 per contract.

You’re saying: “I’m willing to buy Apple at $250 if it drops that low.”

In exchange, you collect a premium upfront.

For this trade, you sold the $250 put expiring March 20 and collected $4.42 per share, or $442 per contract.

That money is yours immediately, regardless of what happens next.

Here’s what happened over the next few days.

As long as Apple stayed above $250, the put kept losing value. That’s time decay — each day the option becomes less valuable, assuming the stock doesn’t move against you. The delta also drifted lower, meaning the option became less sensitive to stock moves. Time worked in your favor every single day.

You didn’t need to watch this happen.

When you opened the trade, you immediately placed a GTC buyback order. For this trade, that meant setting a target to buy back the put at around $1.80.

Why 50% (or in this case, 59%)?

The first half of an option’s premium is the easiest to capture. The second half requires more favorable moves and becomes riskier as expiration nears. By taking profits around 50%, you capture the predictable portion and leave the risky portion for someone else.

Then you’re done. The trade is defined. Entry, exit, and risk are all pre-planned. You set it up once, and the GTC does the rest.

This week, Apple stayed well above $250. By Friday, most of the premium had decayed away, so the system said to take the money and move on.

You closed early, freed the capital, and redeployed it.

That’s how you got roughly 59% profit in four days. The GTC was set at 50%, but the option decayed past the target between sessions — by the time the order filled, the profit was slightly better than planned. That's normal. GTC orders don't always fill at exactly 50%; sometimes the market hands you a few extra points.

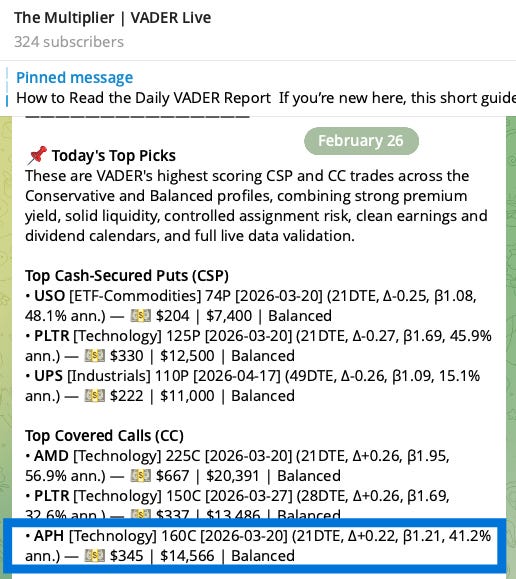

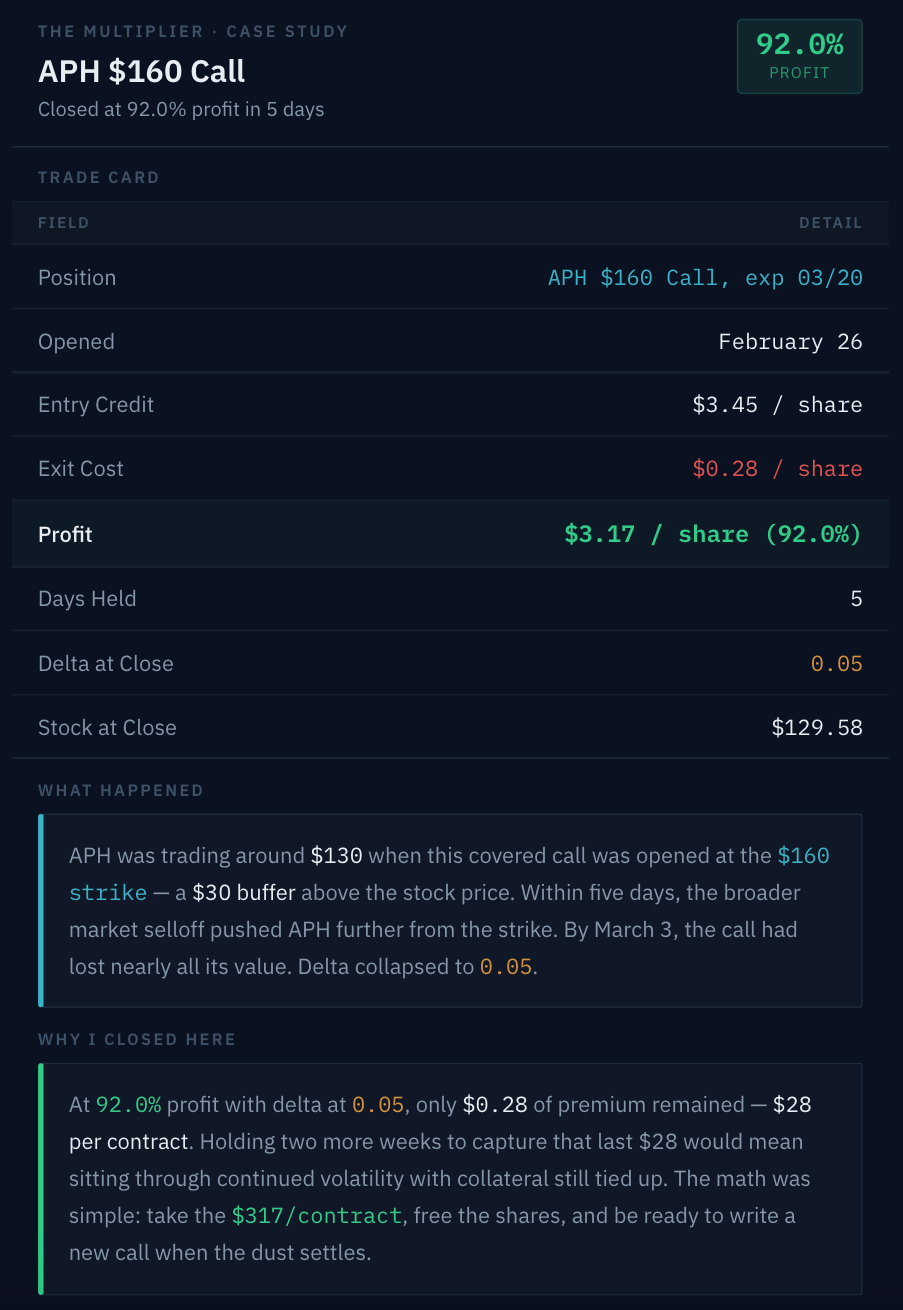

Real Trade Walkthrough #2: APH $160 Covered Call — Closed at 92.0% in 5 Days

Let’s review one of the recent covered call trades.

On February 26, VADER flagged a covered call on Amphenol — the $160 strike, expiring March 20.

What happened

APH was at $130 when this call was opened at the $160 strike — 23% out of the money. Only $3.45 in premium, but the position needed almost nothing to go right.

Five days later, the selloff pushed APH further from the strike. The call lost 92% of its value without APH doing anything special.

Time decay plus falling IV on the call side did all the work.

Why I Closed — And Why I Didn’t Immediately Re-Sell

The close itself was obvious. Delta 0.05, 92% profit, $28 of premium left. Done.

The harder question: what to do with the freed-up shares.

Normally, I would write a new call right away. But after a sharp selloff with the VIX in the high 20s, that creates a trap. If the market bounces on de-escalation news, a freshly written call moves in-the-money fast. The shares get capped right when they’re recovering.

The play: close the call, pocket the $317 per contract, wait. Write the next call after the stock finds a floor — not during the panic.

The Takeaway

A covered call is a volatility recycling tool.

Sell into high IV, harvest the rapid decay when the stock drops, then hold unencumbered shares to participate in any recovery.

The discipline is in the sequencing — resist re-selling into the same elevated volatility that just paid you.

What VADER Is Not

VADER is a screening engine. It finds the best candidates. It does not make your decisions for you.

It is not a signal service. You are not meant to copy every trade blindly. The setups are a curated starting point — your job is to match them to your portfolio, your collateral, your risk tolerance, and your income goal.

It is not a black box. You’ve just read how it works — the filters, the stages, the scoring. I explain my reasoning in every Sunday review and every Monday plan. You see the same trades I manage, the same decisions I make, and the same math I use.

It is not another screener that hands you 200 results and wishes you luck. The entire point is curation. Ten to thirty setups per day, pre-filtered, pre-scored, organized by risk tier and collateral size. Your only job is selection and sizing.

It is not day trading. The typical hold period is 20–45 days. Most members check the channel once in the morning, place an order (or don’t), and move on.

VADER finds the candidates. You make the decisions.

VADER is one part of the premium membership. For the full list of what's included — model portfolios, the Monday plan, the Sunday trade review, and the complete options education library — see What's Included in Premium.

How to Get Access to VADER

Every position reviewed in the walkthroughs above started as a VADER scan setup during the week. Premium members receive those setups in real time, Monday through Friday, in the private Telegram channel.

If you’d like to receive my best hand-selected covered call and cash-secured put setups daily, consider becoming a premium member for $299/year or $49/month.

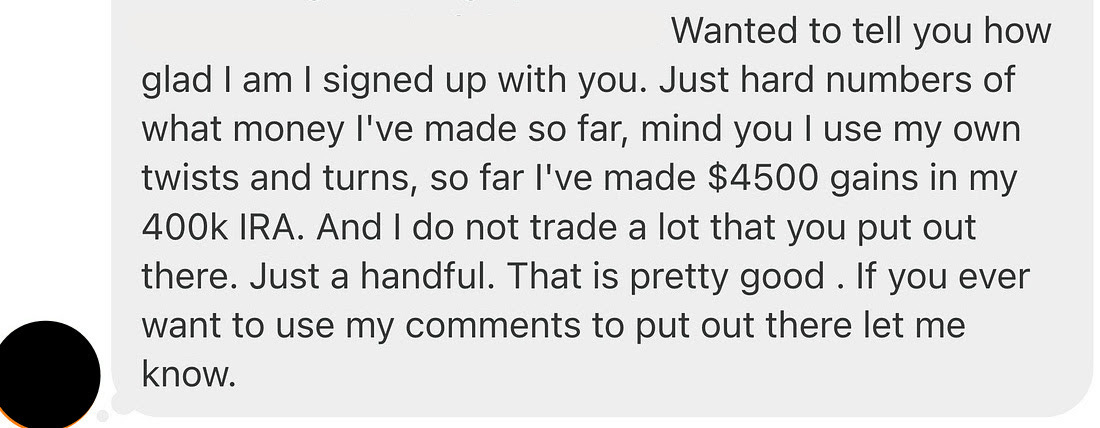

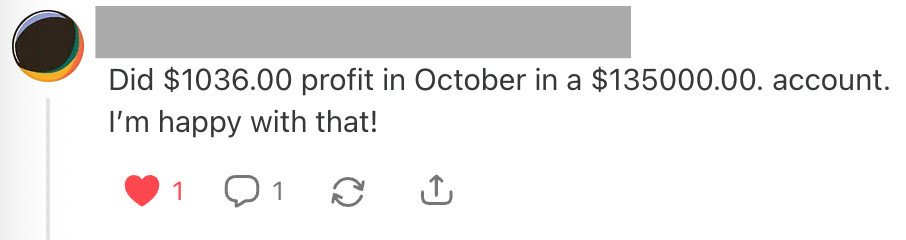

Here is what members are doing in their actual retirement accounts:

There is no risk in giving it a try.

You can cancel anytime.

If you are not satisfied, you can get a full refund within 60 days — just email mike@themultiplier.co.

Hundreds of members have already signed up, and you can read what they have to say.

Most options scanning services charge $500-$1,000 per year and still require you to do the analysis yourself. The Multiplier includes the algorithm, the daily setups, the weekly management plan, and the full education library for $299/year.